With 98% of Canadian businesses being small (many of them owner-managed) and about 68% and 50% (in provinces) requiring structured financial information every year, compilation engagement represents a stable and significant revenue stream for Canadian CPA firms.

Then there is the cross-selling opportunity: compilation engagements provide regular visibility into a client’s financial position. One that makes it easier for you to pitch your other services (bookkeeping, tax planning, and advisory support).

But all of these depend on your ability to deliver compliant service at scale.

As low-effort as Compilations Engagements are (compared with reviews and audits), several CPA firms struggle with keeping them compliant, largely due to the transition from the old Notice to Reader (NTR) to CSRS 4200 in December 2021.

From modernized language and increased documentation requirements to clearer disclosure of the accounting basis and formal acceptance procedures, the new requirements have made it easier for firms managing multiple files to overlook key steps, which highlights the need for a structured workflow in and of itself.

This guide explains what compilation engagements are, when they’re appropriate, and how Canadian firms can deliver them consistently to improve client satisfaction and revenues.

What Is a Compilation Engagement?

The Canadian Standard on Related Services (CSRS 4200) defines a Compilation Engagement as an engagement in which a licensed chartered professional accountant (CPA) assists management in organizing and presenting financial information using an applicable financial reporting framework, without verifying the accuracy of the information or providing assurance on that information.

The goal is to provide management with financial statements that can be used for internal or external purposes, such as:

- Lender requirements for financial statements (without assurance).

- Shareholders’ request for formal year-end financial statements.

- Management’s need for structured financial reports for planning or tax filing.

All you (the practitioner) are required to do is to apply basic knowledge of the entity to identify and address any obvious material misstatements and issue a Compilation Engagement Report that clearly communicates these limitations.

What a Compilation Engagement Is Not

a. Not an audit

An audit engagement involves extensive procedures, including testing transactions and balances, evaluating internal controls, obtaining audit evidence, and assessing the risk of material misstatement.

A compilation engagement does not involve any of these. The practitioner neither performs testing, obtains audit evidence, nor expresses an opinion. Instead, they assist management in presenting financial information based on the information received.

b. Not a review

A review engagement provides limited assurance after performing inquiry and analytical procedures to assess whether the financial statements are plausible and free from material misstatement.

A compilation engagement does not involve inquiry and analytical procedures designed to detect material misstatement. There wouldn’t be a “nothing has come to our attention” statement, since no assurance procedures were performed in the first place.

c. No assurance provided

Under CSRS 4200, the practitioner’s report must state that no assurance is provided, that no opinion or conclusion is expressed, and that the financial statements may not be suitable for purposes other than those intended.

This ensures that users understand the limitations of the compiled financial information and use it appropriately.

d. No verification or audit procedures

In a compilation engagement, the practitioner’s role is limited to organizing financial information into a standard statement format.

You should not verify source documents, test transactions, assess internal controls, or evaluate fraud risk, so the financial statements reflect the information provided by management.

Comparison Overview

| Aspect | Compilation (CSRS 4200) | Review (CSRE 2400) | Audit (CAS) |

| Level of Assurance | None | Limited | Reasonable |

| Procedures Performed | Compiles from client data, uses basic entity understanding, and identifies obvious issues only. | Inquiries and analytical procedures | Extensive testing, evidence, and control assessment |

| Verification | None | Limited | Full |

| Practitioner’s Conclusion | No opinion or conclusion | Limited conclusion on fairness | Opinion on fair presentation |

| Typical Use | Internal management, basic lender needs, and tax support | Mid-level creditor requirements | Regulatory, large loans, public/investor needs |

| Report Wording | Explicitly states “no assurance” and no verification | “Nothing came to our attention…” | “In our opinion…” |

When Is a Compilation Engagement Appropriate?

1. Owner-managed businesses

Compilation engagements are appropriate for owner-managed businesses, where management is directly involved in daily operations and has full knowledge of the underlying financial records.

This means they can verify the information themselves. A compilation engagement gives them professionally formatted financial statements for internal review, planning, or tax purposes, without the expense of a review or audit.

2. Internal management reporting

Businesses also need professionally prepared financial statements for budgeting, performance analysis, or strategic planning.

In that case, management understands that no assurance will be provided. They need compiled financial statements to give their financial information the right structure.

3. Tax preparation support

Some businesses request compilation engagements prepared alongside their corporate tax return (T2) because the financial statements align with tax calculations, which streamlines the corporate return process.

4. Shareholder reporting (where assurance isn’t required)

For many private companies, a compilation engagement is adequate for shareholder reporting when there is no regulatory requirement, and the shareholders understand that no assurance is provided.

Family-owned businesses are a good example. Compilations are usually sufficient because shareholders are involved in day-to-day operations and can obtain information directly from management.

5. Small business financing scenarios

Many Canadian lenders accept compiled financial statements for loans or lines of credit under $1–2 million, especially when they have an established relationship with the business owner and can obtain further details if required.

In such cases, compilations are a cost-effective alternative to reviews or audits.

When a compilation may not be appropriate:

A higher level of assurance, such as a review or audit, is needed when:

- Regulatory or contractual obligations require it.

- The business is complex or high-risk, and external stakeholders cannot access or verify financial information directly.

- Users require greater confidence, such as in litigation, business acquisitions, or when parties unfamiliar with the company rely on the financial statements.

Key Requirements Under CSRS 4200

-

Engagement acceptance and continuance

Under CSRS 4200, the practitioner must evaluate whether a compilation engagement is appropriate before accepting or continuing a compilation engagement.

This involves:

-

- Understanding the entity and ensuring that the management acknowledges its responsibilities for the accuracy and completeness of the financial information.

- Determining intended users, the purpose of the compilation, and any potential third-party users.

- Getting management’s acceptance of the basis of accounting to be used in the engagement.

If these conditions are not met (or an agreement cannot be reached with management), you should withdraw from the engagement. Otherwise, document the considerations in the engagement letter and proceed.

-

Understanding the entity and accounting basis

CSRS 4200 requires the practitioner to obtain an understanding of the entity, its business operations, accounting records system, accounting policies, and the basis of accounting applied in the financial statements.

This knowledge enables you (the practitioner) to compile financial statements that are not misleading.

-

Management’s responsibility acknowledgment

Under CSRS 4200, the management’s acknowledgement of responsibility for the financial information is non-negotiable.

This includes responsibility for the accuracy and completeness of the underlying records, the selection of the appropriate basis of accounting, and the prevention and detection of fraud.

-

Compilation engagement report requirements

Another requirement to meet carefully is the attachment of a Compilation Engagement Report to the financial statements.

While the report does not include an opinion or conclusion paragraph, it does:

-

- Identify the financial information that has been compiled.

- Describe the practitioner’s role and management’s responsibilities.

- Include a caution regarding the basis of accounting and the intended use of the compiled financial information.

- Have a signature and date.

The language or wording of the report must clearly communicate the limitations of a compilation engagement.

-

Required note disclosures (including basis of accounting)

Although the CSRS 4200 does not require full note disclosure, the compiled financial statements must include sufficient information to help users understand how the statements were prepared, the applicable financial reporting framework, including any significant limitations.

This disclosure of the basis of accounting minimizes, if not eliminates, ambiguity in the compiled financial information, which was common in the Notice to Reader period.

-

Documentation expectations

Although compilation engagements are lower risk than audits and reviews, they are no longer treated as informal exercises.

Regulators and practice inspectors expect practitioners to maintain appropriate documentation to demonstrate that:

-

- The engagement was properly accepted.

- The basis of accounting was determined.

- Management responsibilities were acknowledged.

- The financial information is not misleading.

- Professional judgment was applied.

You can take advantage of resources like the CPA Canada’s PACT guide, PEG templates, or provincial CPA resources to ensure compliant documentation processes.

The Compilation Engagement Process (Step-by-Step)

This step-by-step Compilation Engagement process draws insights from CPA Canada’s practice management, advisory, compilations, and tax guide (PACT).

Step 1: Client acceptance and engagement letter

Before beginning any compilation engagement, you must determine whether the engagement is appropriate under CSRS 4200 guidelines to prevent accepting unsuitable engagements.

This entails identifying the intended users of the compiled financial information, agreeing with management on the applicable basis of accounting, and confirming that management understands that no assurance will be provided.

Once you find that a compilation engagement is appropriate, send an engagement letter that outlines the details you already identified (such as the purpose and intended users) and the agreement reached with the management on responsibilities.

Step 2: Identify the basis of accounting

This step includes ensuring the selected basis of accounting is suitable for the intended purpose of the compilation engagement and that the management has agreed with it.

This could be Accounting Standards for Private Enterprises (ASPE), cash basis, tax basis, modified cash basis, or another special purpose framework.

You should also discuss any significant judgments that may affect the financial statements (such as estimates related to accruals or allowances) with the management.

Step 3: Gather financial information

This is where you collect the financial information necessary to prepare the compiled financial statements.

This information usually includes trial balance, bank statements, supporting schedules, and adjusting journal entries (where applicable).

Step 4: Compile financial statements

Organize the financial information provided by management into formal financial statements, which could include a statement of financial position, statement of operations, statement of changes in equity, statement of cash flows (if applicable under the chosen framework), and accompanying notes.

While you are not performing audit or review procedures, you should be alert to obvious errors, inconsistencies, or questionable relationships that become apparent during the compilation process.

If the information provided appears incomplete, inconsistent, or potentially misleading, you are required to discuss the matter with management before proceeding. If the issue cannot be resolved, you should decline to issue the compilation engagement report.

Step 5: Include required disclosures and notes

Add a note describing the basis of accounting used to prepare the compiled financial statements.

Where necessary, you may also include disclosure of significant accounting policies, key judgments made by management, or limitations that are common with the chosen basis of accounting.

Because the management is responsible for the financial information, you should obtain management’s acknowledgment and approval of the final financial statements before issuing the compilation engagement report.

These disclosures are important for users who need to understand the nature of the financial information and its special-purpose or non-GAAP basis.

Step 6: Prepare and issue the compilation engagement report

The compilation engagement report is a crucial aspect of the CSRS 4200 standard. It communicates the nature and limitations of the work performed and prevents users from misunderstanding the financial information.

The report should:

- Identify the compiled financial information.

- Describe management’s responsibility for the financial information.

- Describe the practitioner’s role in the compilation.

- State that no audit, review, or other assurance engagement was performed.

- Refer to the note describing the basis of accounting.

- Be signed and dated by the practitioner.

The wording of the report must follow the format prescribed by CSRS 4200 and not suggest that any assurance is being provided. Once finalized, attach the compilation engagement report to the compiled financial statements.

Step 7: Final review and delivery

This final review of the file is performed to ensure that all CSRS 4200 requirements have been met.

Your focus here is to confirm whether:

- The compiled financial information has been properly organized and presented.

- The required note, which describes the basis of accounting, is included and accurately reflects the agreed-upon framework.

- Sufficient disclosure has been provided to prevent the financial information from being misleading.

- The compilation engagement report follows the prescribed wording and format.

- The file documentation supports the engagement acceptance, the basis of accounting, and the professional judgments applied.

Once finalized and dated, you (the practitioner) can deliver the compiled financial statements, notes, and the Compilation Engagement Report to management.

PRO TIP:

Retain all engagement documentation, including the signed engagement letter, management acknowledgments, understanding of the entity, working papers, and the final issued statements and report to meet relevant data retention requirements.

Free Checklist Templates (Canada)

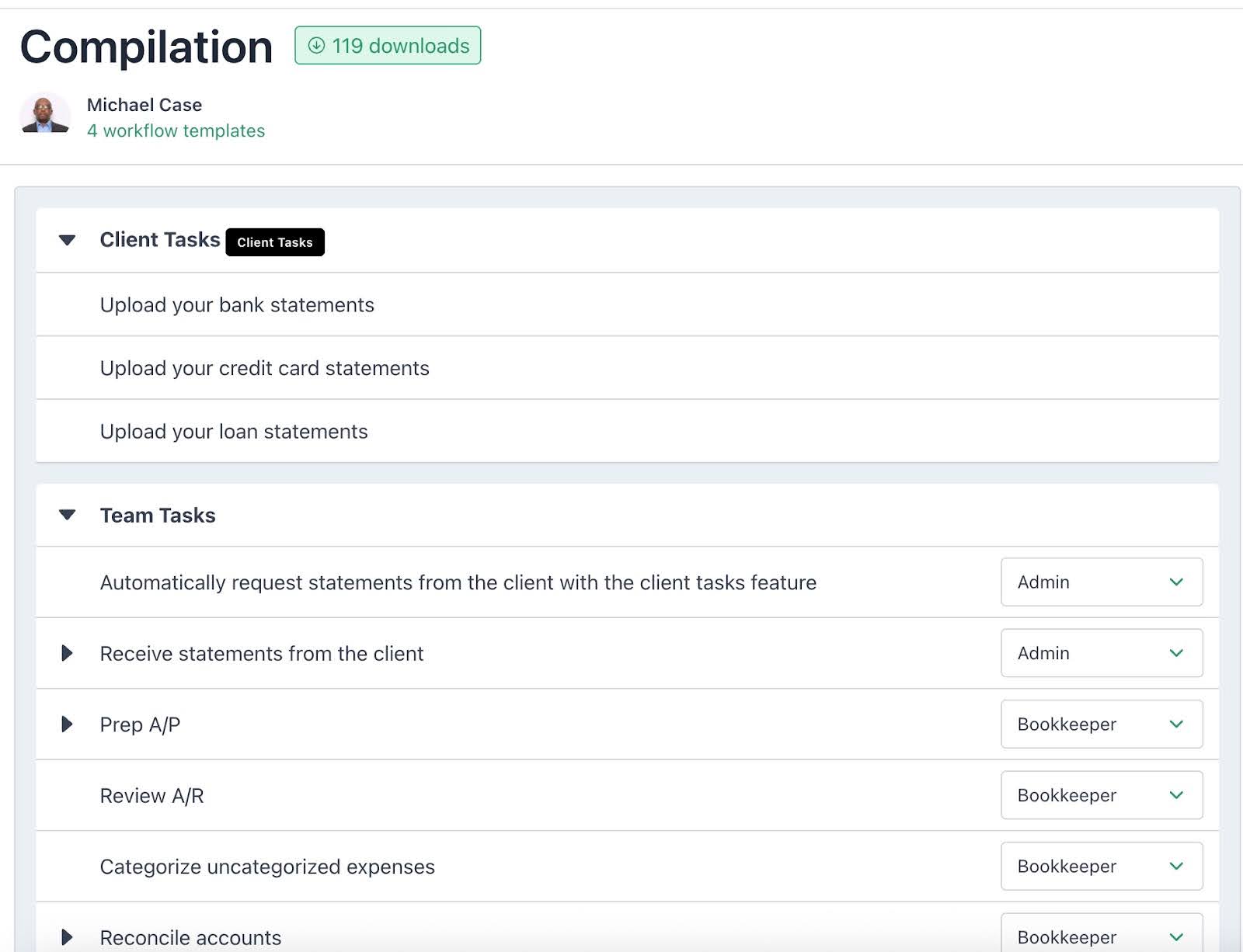

A. Compilation

Click here to download the template

Built by Michael Case of Case of Case CPA Professional Corporation, this Compilation Checklist Template has 10 team tasks, three (3) client tasks, and three (3) assignee roles (Admin, Bookkeeper, and Reviewer).

It relies on 6 tag automations in Financial Cents to spare the practitioners manual labor and give them more time to deliver compliant service.

The template has been downloaded by 119+ other accounting firms, which indicates its popularity among other Canadian chartered professional accountants (CPAs).

You can customize the checklist to meet all CSRS requirements by adding more steps, like

- Document engagement acceptance/continuance.

- Obtain management acknowledgments.

- Include basis-of-accounting notes.

- Prepare the Compilation Engagement Report.

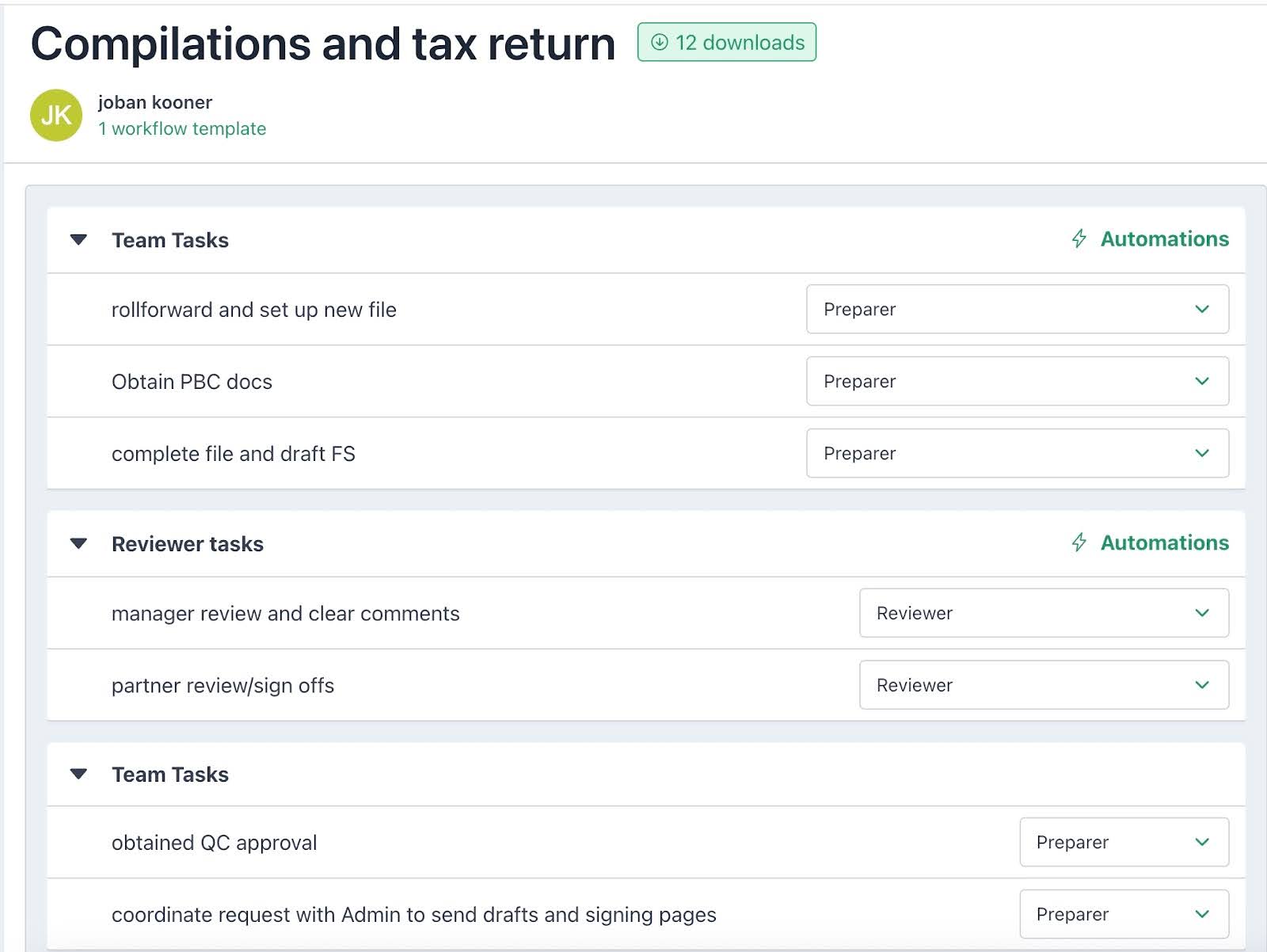

B. Compilations and Tax Return

Click here to download the template

Joban Kooner of Zeifmans LLP created this template for Canadian CPAs providing Compilation Engagements and corporate tax returns (T2). It helps them to improve visibility across their engagements.

The template has 12 tasks, which are assigned to the Preparer, Reviewer, and Admin. It also applies Financial Cents automations in four stages of the work to change the status of the work without manual effort.

The template may require customization with CSRS-mandatory steps, like engagement letter issue, entity understanding documentation, basis-of-accounting note, and the Compilation Engagement Report.

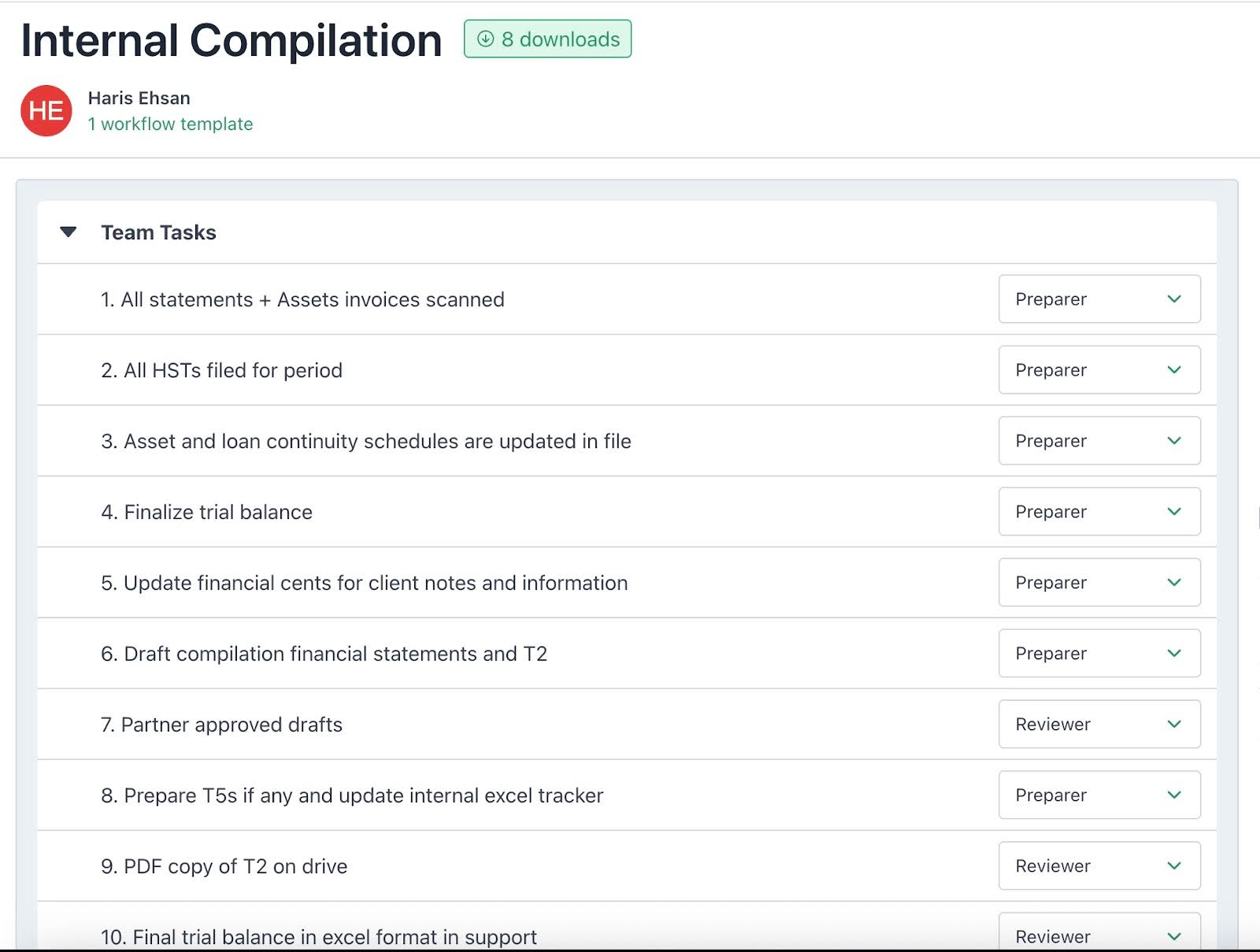

C. Internal Compilation

Click here to download the template

Haris Ehsan’s (of SECPA Professional Corporation) workflow template is explicitly designed as an internal checklist for Canadian CPAs.

The template serves as a linear, high-level checklist for the internal wrap-up and quality control phase of a compilation engagement, often bundled with corporate tax return (T2) preparation and filing.

Its inclusion of HST, T2, T5, and T183 in the steps makes it helpful for Canadian firms handling year-end compilations that feed directly into T2 corporate tax returns.

Common Pitfalls & Compliance Risks

These are the most frequent aspects of the compilation engagement that practitioners struggle with (according to the practice inspections of several provincial CPA bodies):

Using outdated Notice to Reader language

Some firms, accustomed to the former NTR format, accidentally use the old Section 9200 report language and standard instead of the prescribed Compilation Engagement Report required in CSRS 4200.

This error can mislead users regarding the nature and limitations of the engagement and may expose the firm to regulatory findings during practice inspections.

To address this risk, practitioners should:

- Update their templates to CSRS 4200–compliant language.

- Clearly state that no audit, review, or assurance engagement was performed.

- Include the required reference to the note describing the applicable basis of accounting.

Missing required disclosures

Some practitioners omit the basis of accounting note entirely, while others include vague or incomplete disclosures that fall short of explaining how the financial information was prepared.

For example, when the financial statements state they were prepared “in accordance with Accounting Standards for Private Enterprises (ASPE)” but fail to include key elements required under ASPE (like the required note disclosures), the financial information is not consistent with the stated framework.

This violation renders the report misleading, non-compliant, and exposes your firm to professional liability.

Experienced practitioners often implement standardized disclosure checklists to remind practitioners to document:

- Basis of accounting.

- Significant accounting policies.

- Review points that ensure financial statements are consistent with the framework used.

Third-party misuse of compiled financials

Compilation engagements are performed for a specific intended use and users, which is agreed upon at the acceptance stage.

However, a recurring risk arises when lenders, investors, or other third parties treat compiled financial statements as if they were subject to review or audit procedures.

Because a compilation provides no assurance, third parties who misunderstand the engagement may assume that the practitioner has verified balances, assessed internal controls, or performed analytical procedures.

If financial difficulties arise on such an account, the users may claim reliance on the statements, which will call the practitioner’s role into question.

It doesn’t help that some practitioners have accepted a compilation engagement in circumstances where management or a third party actually required assurance in the past.

You (as the practitioner) must manage expectations by:

- Conducting thorough inquiries regarding intended users and intended use at the engagement acceptance stage.

- Documenting these discussions in the engagement letter.

- Ensuring the compilation engagement report uses the standard wording to describe the purpose of the financial information.

- Avoiding assumptions that “small lenders only require compilations” without direct confirmation.

Inadequate documentation

Many practitioners also miss the minimum documentation requirements of the CSRS 4200.

They provide insufficient evidence of engagement acceptance, inadequate records of the practitioner’s knowledge of the entity, failure to document independence considerations, or reconciliation of the underlying accounting records to the compiled financial information (CFI).

Poor documentation is usually caused by reliance on memory or outdated filing habits and can cause compliance violations during practice inspections.

Experienced practitioners maintain a comprehensive engagement file (including signed engagement letters, working papers, and final reports).

You should also document any discussions with management regarding incomplete or inconsistent data.

Unclear engagement scope

When practitioners fail to adequately document compilation engagements, they expose their firms to practice inspection deficiencies, compliance failures, and weakened defense in the event of disputes or liability claims.

Experienced practitioners address this by maintaining a comprehensive engagement file that includes:

- Signed engagement letters and management acknowledgments.

- Working papers supporting compiled balances.

- Notes on understanding of the entity and accounting system.

- Records of discussions with management regarding incomplete or inconsistent data.

- The final compiled financial statements and compilation engagement report.

Thorough documentation demonstrates that the engagement was performed in accordance with CSRS 4200 and supports professional judgment applied throughout the process.

Ensure Clarity, Compliance, and Consistency in Every Engagement Using Financial Cents Practice Management Solution

Compilation engagement remains a critical service for Canadian CPAs. But since the 2021 transition from Notice to Reader to CSRS 4200, the work has gone from low-risk work to a structured service that requires greater consistency and documentation, and that has been particularly difficult for firms coming from old NTR habits.

The growing need for firms to standardize procedures, centralize information, and automate client data collection calls for the right accounting practice management software to keep multiple compilation engagements compliant.

Firms using Financial Cents, for example, save 56 hours per team member every month, get client documents six (6) times faster, and consolidate in one tool the multiple apps.

Its accounting-specific features include:

- Workflow Management and Automation: Ensures all CSRS 4200 steps are consistently followed, deadlines are met across the board, and manual tasks are automated.

- Client Portal: Centralizes and automates client data collection and collaboration.

- CRM and Database: Stores all the client information you need to demonstrate sufficient knowledge of their business entity.

- Proposals and Engagement Letters: Enable you to define scope, establish responsibilities, and align expectations between your firm and clients.

- Billing and Payments: Streamline billing and payment, where work is getting done, to minimize late invoicing and payments.

See how Financial Cents can make your compilation engagements and your entire accounting, bookkeeping, and tax operations more organized, efficient, and compliant today.