Financial accuracy is the cornerstone of trust between an accounting firm and its clients. After all, maintaining a strong reputation hinges on delivering reliable financial information to your clients.

But how do you maintain consistency and minimize errors when handling a growing number of clients and a constantly evolving regulatory landscape?

Enter: a well-defined set of accounting policies and procedures (P&Ps).

Imagine your P&Ps as a detailed roadmap, guiding your team through every step of the accounting process, from processing invoices to generating reports. It ensures everyone is on the same page, using the same tools, and adhering to the same high standards. This consistency minimizes errors and maximizes efficiency – a win-win for your firm and your clients.

In this guide, you’ll learn everything about a P&P manual plus a free template so you can create one for your firm.

What are Accounting Policies and Procedures?

Accounting policies are the principles and methods your firm adopts to prepare financial statements. They act as the overarching guidelines that dictate how you account for various financial elements like asset valuation, revenue recognition, and expense recognition.

Think of accounting policies as the guiding principles that define your firm’s approach to financial reporting. These policies provide the “why” behind your financial reporting, dictating how you handle various financial elements like:

- Asset valuation: FIFO (first-in, first-out) or LIFO (last-in, first-out) method to value inventory. Or the straight-line or accelerated depreciation method for fixed assets.

- Revenue recognition: when to record income based on industry practices.

- Expense recognition: determining appropriate timing to record expenses.

On the other hand, accounting procedures are the step-by-step instructions that translate the broad principles into practical actions. They answer the “how” by outlining specific tasks your team performs throughout the accounting cycle. Procedures might include:

- Transaction coding: sales, purchases, payroll

- Invoice processing

- Account reconciliation

- Closing the books

Now, the question: Is there a difference between accounting policies and accounting procedures? Yes, there is.

Accounting policies provide the foundation (the “why”), while accounting procedures ensure consistent execution (the “how”). They are two sides of the same coin, working together to ensure accurate and consistent reporting for your firm.

Benefits of Policies and Procedures for Accounting Firms

There are many benefits to having a documented P&P for your firm. They include:

a. Improved Efficiency

Streamlined procedures save time and resources by eliminating confusion about who/how to handle different accounting tasks. When team members know exactly what’s expected of them, they can complete projects faster, enabling them to work more efficiently.

b. Stronger Internal Controls

Your internal control framework helps maintain the integrity of your client’s data and protects their assets. To strengthen this framework, you need to define your P&Ps. Procedures can outline the division of duties, access controls, and documentation standards, creating a more secure financial environment.

c. Effortless Onboarding and Training

New team members can quickly grasp your firm’s financial practices by referring to a comprehensive P&P manual. This reduces training time and ensures everyone is on the same page from day one. Consistent application of procedures also reduces the risk of errors made by new hires.

d. Simplified Regulatory Compliance

Clear P&Ps help ensure your firm adheres to relevant accounting standards and industry regulations. This reduces the hassle of scrambling to meet compliance requirements and the risk of penalties or fines.

e. Boosted Client Trust and Confidence

With a standardized procedure, you’ll be able to create more reliable financial statements for your clients. This will give them peace of mind, increase their trust in you, and improve your relationship with them.

Key Components to Include in Your Accounting Firm’s Policies and Procedures Manual

Now that you’ve seen the benefits of an accounting P&P and why you should have one, let’s look at what to include in yours.

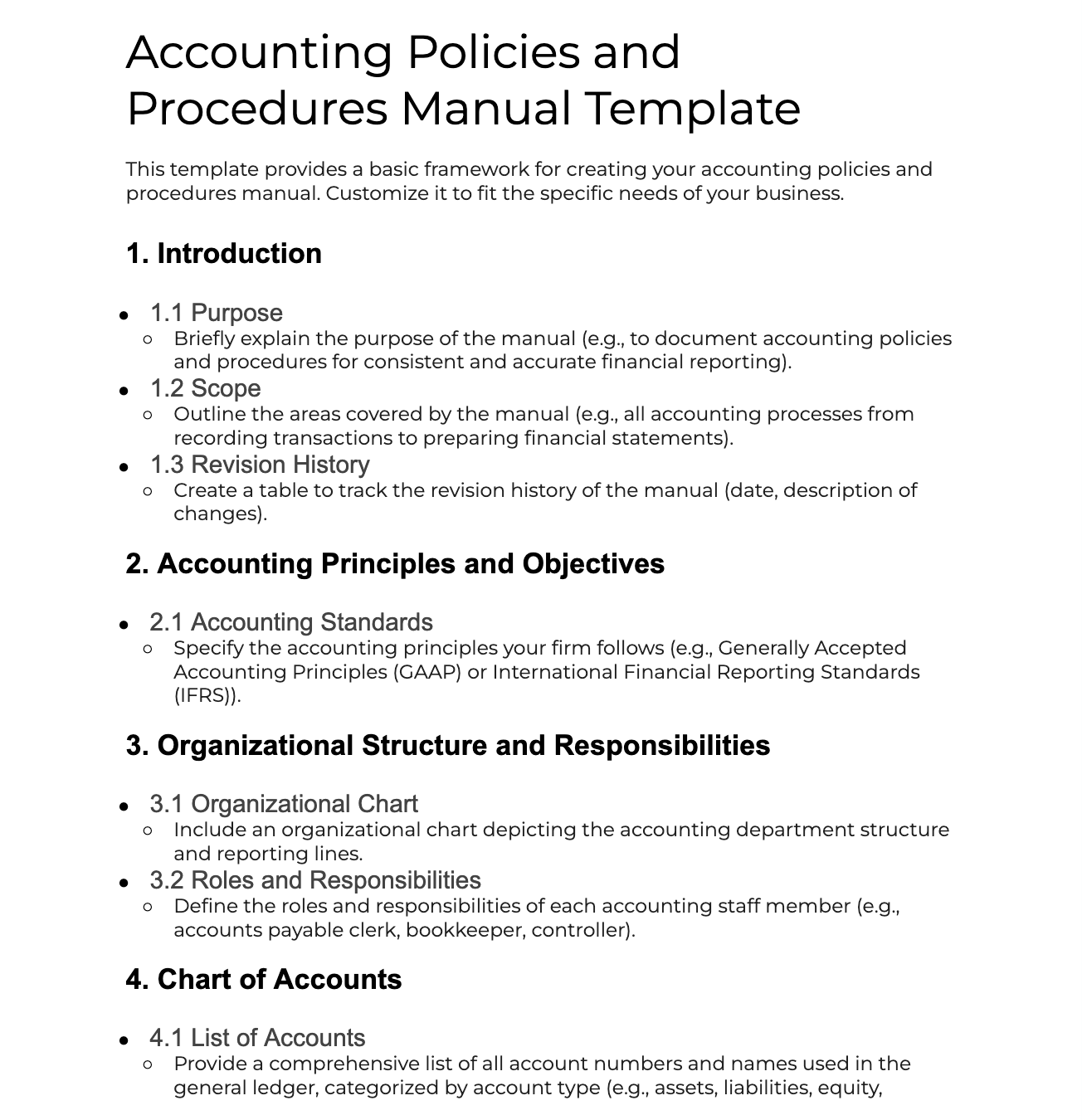

a. Introduction: This section provides a brief overview of the manual’s purpose and scope. It should also outline who the manual is intended for (staff, clients, etc.) and how often you’ll review and update it.

b. Accounting Principles and Objectives: Here, clarify the accounting framework your firm adheres to, e.g., Generally Accepted Accounting Principles (GAAP) or International Financial Reporting Standards (IFRS). Also, outline the key objectives of your accounting practices, such as accuracy, consistency, and compliance.

c. Organizational Structure and Responsibilities: Clearly define the roles and responsibilities of each team member involved in the accounting process. This includes outlining approval hierarchies and segregating duties for robust internal controls.

d. Chart of Accounts: This is a list of all the accounts used in your general ledger, categorized into specific accounts for tracking and reporting purposes. Provide clear descriptions for each account for accurate classification of income, expenses, assets, and liabilities.

e. Transaction Procedures: Detail the step-by-step process for handling different types of transactions, such as sales, purchases, cash receipts, and disbursements. Include specific instructions for handling unusual or complex transactions.

f. Revenue Recognition: Define the criteria your firm uses to recognize revenue from different sources, such as product sales, service provision, or other revenue streams. This will depend on the specific industry and the nature of your client’s business. For example, service-based businesses typically recognize revenue when they render the service, while product-based businesses recognize revenue when they deliver the product. Proper revenue recognition practices are essential for demonstrating the financial performance of your firm.

g. Expense Recognition: Outline the methods used to recognize and record expenses incurred in the course of your firm’s operations. This includes administrative costs, marketing expenses, and overhead expenditures. Also, specify how you handle prepaid expenses and accrued liabilities.

h. Financial Reporting: In this section, explain the processes and requirements for preparing financial statements, like the balance sheet, or income and cash flow statements. Then detail the procedures for preparing and distributing these reports internally and to clients. This will help clients understand their financial performance and position.

i. Closing Periods: Define the procedures for closing the books at the end of an accounting period, including journal entries, account reconciliations, and inventory adjustments. Properly closing accounting periods helps in identifying any discrepancies, resolving issues promptly, and ensuring reliable financial reporting/analysis.

j. Internal Controls: Establish a framework for internal controls to protect your firm’s assets and ensure data integrity. This includes procedures for access control, transaction authorization, record retention, and data backup.

k. Compliance and Regulations: Outline any relevant industry regulations or external reporting requirements that your firm must comply with to avoid penalties. Examples include tax regulations or industry-specific reporting standards.

I often discover new regulatory changes through client interactions or unexpected events, and sometimes, I’m surprised by what comes up. I also stay informed by watching IRS videos—they have quite a good selection on their website. Additionally, continuing professional education (CPE) webinars are essential for training. However, I frequently consult with the attorneys I work with to get their perspectives on new developments. Eric Green has been an invaluable resource for understanding upcoming regulatory changes, and I’ve learned much from him."

Dawn Brolin, CEO, Powerful Accounting LLCl. Documentation: State the standards for documenting accounting processes and transactions. This includes guidelines for the format and retention period for invoices, receipts, and other supporting documents, record-keeping practices, and the importance of documenting the rationale behind financial decisions. Comprehensive documentation not only ensures transparency and accountability but also facilitates auditing processes and internal reviews to validate the integrity of the financial data stored. You may also need a document management system.

m. Reporting and Communication: Enforce communication protocols regarding accounting matters within the firm and with clients. This could include procedures for client inquiries, issue escalation, and reporting deadlines.

n. Updates and Revisions: Accounting standards and regulations can evolve over time. So, set up a process for reviewing and updating your P&P manual to ensure it remains current and reflects best practices.

o. Training and Onboarding: Finally, explain the strategies and methods you’ll use to introduce new employees to the company and prepare them for their roles. Include the orientation process, which acquaints newcomers with the firm’s operational standards, culture, and expectations, as well as comprehensive training programs tailored to specific roles within the firm. Also, detail the ongoing professional development opportunities available to all employees to ensure they remain proficient in their respective areas.

Free Accounting Policies and Procedures Template

Here’s what our accounting P&P template looks like:

Free Accounting Policies and Procedures Template

Conclusion

Having a well-defined set of accounting P&Ps is not a recommendation, it’s a must-have for your firm. These documented guidelines help streamline workflows and ensure your financial reporting is consistent and accurate.

Furthermore, being known for having a standardized process boosts your reputation and can help you attract more clients.

To further increase your firm’s efficiency, check out Financial Cents. Our tool helps you manage your company’s processes, collaborate seamlessly with your team and clients, and automate time-consuming tasks.

Use Financial Cents for your workflow management.