A Canadian T2 corporation income tax return has more moving parts than any other return your firm files. GIFI schedules, Schedule 1 reconciliations, the Small Business Deduction limit, capital cost allowance continuity, RDTOH and GRIP balances, provincial allocation, EIFEL interest limits, investment tax credits, related-party disclosures, one missed schedule or one un-flagged shareholder loan is a CRA review notice and a reassessment six months later.

This free T2 corporation tax return checklist template gives Canadian CPAs and tax preparers a single working document that covers the entire engagement from kick-off to EFILE, ten sections, every required schedule called out, and explicit sign-off rows that make review a hard gate rather than a polite suggestion.

It’s built specifically for firms running T2 engagements at scale, the kind of practice where consistency across preparers, defensible working papers, and on-time filing matter more than any single accountant’s memory of which schedules apply to a CCPC versus a professional corporation versus an NPO.

What’s Inside the T2 Corporation Tax Return Checklist Template

The template is a fully editable Google Sheets / Excel file structured into ten sections that follow the natural flow of a corporate tax engagement:

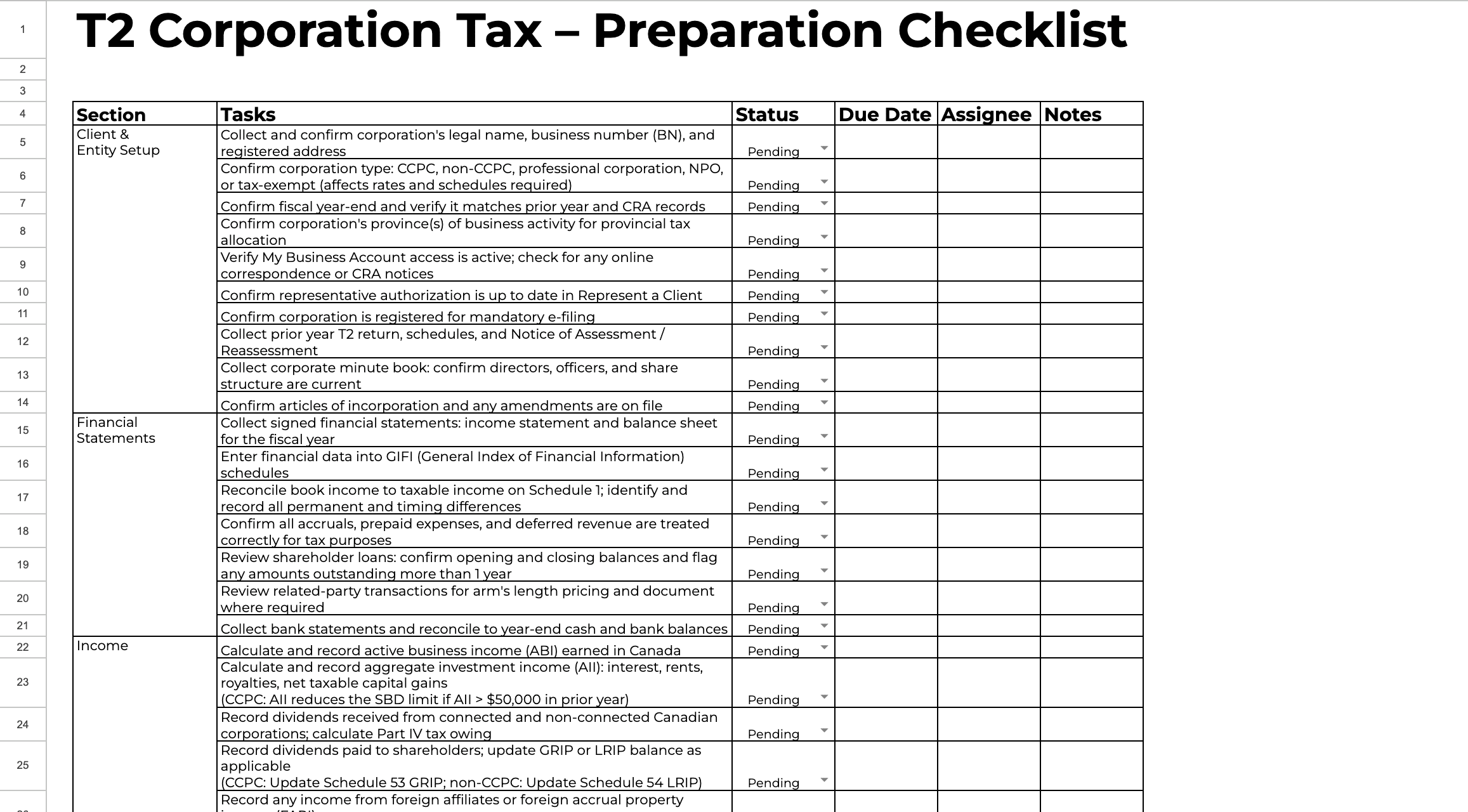

- Client & Entity Setup: Legal name, Business Number, registered address, corporation type (CCPC, non-CCPC, professional corporation, NPO), fiscal year-end confirmation, My Business Account access, Represent a Client authorization, mandatory e-filing registration, prior-year T2 and NOA, corporate minute book review.

- Financial Statements: Signed F/S, GIFI data entry, Schedule 1 book-to-tax reconciliation, accruals and deferred revenue tax treatment, shareholder loan continuity, related-party transactions, bank reconciliation.

- Income: Active business income, aggregate investment income (and its SBD-limit impact), inter-corporate dividends and Part IV tax, dividends paid with GRIP/LRIP tracking, foreign affiliate income / FAPI, rental income, capital gains and Schedule 6.

- Deductions & Expenses: Operating expenses, CCA continuity by class, capital cost incentives, charitable donations and the 75% net income limit, reserve continuity, non-deductible expenses (50% meals, fines, non-arm’s length payments), loss carry-forwards, EIFEL compliance on interest and financing.

- Small Business Deduction (CCPC): CCPC qualification confirmation, active business income calculation, business limit and any reductions (passive investment income, taxable capital), Schedule 23 for associated corporations, federal SBD rate, provincial SBD rates.

- Investment Tax Credits: SR&ED, Clean Technology ITC, Clean Technology Manufacturing ITC, Carbon Capture Utilization and Storage ITC, Clean Hydrogen ITC, EV Supply Chain ITC, ITC carry-forwards, labour-requirement attestation for clean economy credits.

- Related Parties & Shareholders: Schedule 9 disclosures, Schedule 11 transactions, shareholder loans receivable and the 1-year rule, shareholder loans payable, reasonable management fees, tiered structure Part IV review, non-arm’s length Schedule 44, transfer pricing documentation.

- Corporation-Type Specific Items: CCPC refundable Part I tax and RDTOH updates, GRIP on Schedule 53, professional corporation personal-services-business checks, NPO T1044 filing thresholds, non-CCPC SR&ED eligibility, large-corporation Schedule 45 taxable capital, MNE Global Minimum Tax registration triggers.

- Provincial & Territorial Tax: Schedule 5 allocation, provincial rates and small business limits, provincial tax credits, Quebec separate filing with Revenu Québec, Alberta AT1 with ATA.

- Filing & Sign-Off: 6-month filing deadline, 2- or 3-month payment deadline, instalment reconciliation, direct deposit, EFILE transmission with T183CORP, voluntary disclosure considerations, secure client delivery, carry-forward schedule update, 7-year working paper retention, preparer and manager sign-off.

Every row includes Status, Due Date, Assignee, and Notes columns, so the checklist works as a standalone engagement file or as a project template inside a practice management system.

Why Every Canadian Firm Needs a T2 Checklist Template

T2 returns are where firms lose money and rack up risk simultaneously. The volume is lower than T1 but the consequences of an error are bigger, SBD limit miscalculations get reassessed, missed shareholder loan inclusions trigger subsection 15(1) issues, ITC eligibility decisions get audited years after the fact. The firms that file T2s confidently are the ones with a written process that covers every section, every schedule, and every corporation type.

Three failure modes show up over and over in T2 work. The first is the wrong corporation-type assumption: a CCPC that was acquired by a non-resident and quietly lost CCPC status, a professional corporation that wandered into personal services business territory, an NPO that crossed the T1044 reporting threshold. Each of these changes which schedules apply and which rates flow through. The checklist forces a confirmation in section 1, before any numbers are touched.

The second is the SBD limit miscalculation. The federal $500,000 limit is the easy part. The reductions — for prior-year aggregate investment income above $50,000, for taxable capital above $10M, for the associated-corporation sharing rules on Schedule 23, are where the math gets missed. The Small Business Deduction section calls each one out as a separate line item so nothing is assumed.

The third is the schedule pile-up at filing. T2 returns can require dozens of schedules depending on the corporation. Without an explicit checklist of which schedules apply to which corporation type, a preparer hits the EFILE button and discovers a missing Schedule 53 or Schedule 9 only when the CRA bounces the file. The Filing & Sign-Off section is structured to catch this before the return goes out.

Who This T2 Tax Return Checklist Is For

This template is built for Canadian firms with corporate clients on the books. It’s especially useful for:

- CPA firms preparing T2 returns for owner-managed CCPCs, professional corporations, and holding companies

- Tax-focused practices with high-volume corporate engagements (50+ T2s per preparer)

- Bookkeeping firms expanding into year-end corporate compliance

- Solo practitioners who need defensible working papers in case of a CRA review

- Multi-partner firms standardizing T2 engagements across preparers and reviewers

- Firms onboarding new junior staff who need a step-by-step structure before they can be trusted with a T2 file

If you also handle personal returns, our free T1 personal tax return checklist is the equivalent on the individual side. For US firms preparing 1120 corporate returns, the free 1120 business tax return checklist is the corporate tax variation.

How to Use the T2 Corporation Tax Checklist Template

- Make a copy per corporation per fiscal year. Open the template in Google Sheets, “File → Make a copy,” and rename to include the corporation name and fiscal year-end. Keep the original as your firm’s master template.

- Start with the Client & Entity Setup section. Corporation type, fiscal year-end, CCPC status, and Represent a Client authorization determine which downstream sections apply. Don’t skip this section to get to the numbers faster, the answers here change the work later.

- Run sections in order, but assign sections to roles. Junior staff own Client Setup and Financial Statements; a senior preparer owns Income, Deductions, SBD, and ITCs; the partner or manager owns Related Parties, Corporation-Type Specifics, and the final sign-off. Use the Assignee column to make this explicit.

- Mark status as you go. Pending → In Progress → Done. Reviewers can see exactly which sections are still open without opening the engagement file.

- Treat both sign-off rows as the gate. No T2 leaves the firm without the preparer sign-off and the independent manager / partner sign-off. The CRA expects a documented review; your malpractice insurer expects the same.

For firms with a corporate-tax book of more than a handful of clients, the checklist quickly outgrows the spreadsheet. A tax firm practice management software lets you load the checklist as a recurring project template, attach it to every corporate client’s fiscal year-end automatically, and see every active T2 across the firm on one dashboard.

Common T2 Mistakes This Checklist Helps You Avoid

The mistakes that drive CRA reassessments, late filings, and lost time on T2 work tend to repeat. The checklist is structured to surface each one before EFILE:

- Wrong corporation-type classification. A CCPC that quietly lost CCPC status, a professional corporation drifting into personal services business territory, an NPO above the T1044 threshold, the Client & Entity Setup section forces these checks first.

- SBD limit miscalculation. Forgetting the prior-year aggregate investment income reduction, the taxable capital phase-out, or the Schedule 23 associated-corporation sharing. The Small Business Deduction section calls each one out.

- Shareholder loan timing miss. Loans receivable from shareholders need to be repaid within one year of the corporate year-end or included in the shareholder’s personal income under subsection 15(2). The Related Parties section forces a continuity check.

- Schedule 1 missing differences. Permanent and timing differences between book and tax income drive every CCA, reserve, and non-deductible adjustment. The Financial Statements section requires Schedule 1 reconciliation as a discrete step.

- RDTOH and GRIP not updated. For CCPCs paying dividends, RDTOH and GRIP continuity is the difference between an eligible and non-eligible dividend designation. The Corporation-Type Specific Items section captures this.

- Provincial allocation skipped. Multi-province operations require Schedule 5 even when the income split looks obvious. The Provincial & Territorial Tax section makes this an explicit step.

- Missed filing deadline nuance. The return is due 6 months after year-end; the balance is due 2 or 3 months after. Missing the payment deadline triggers interest even if the return is filed on time. The Filing & Sign-Off section captures both.

- Single-preparer return without independent review. The two sign-off rows enforce a second pair of eyes before transmission.

From T2 Checklist to a Full Corporate Tax Workflow

A checklist standardizes one T2 return. A practice management system standardizes a whole corporate tax book. The firms that move through the wave of December and March year-ends without partner burnout are the ones who’ve turned the checklist into a recurring project template, attached it to every corporate client, and let the system handle deadlines, document chasing, and review assignments automatically.

Financial Cents is the practice management platform Canadian CPAs and tax firms use to run their entire T2 workflow from one dashboard. The checklist can be imported as a project template; deadlines auto-generate from each corporation’s fiscal year-end; client document requests for signed F/S, minute books, and supporting schedules run on auto-reminders so your team isn’t chasing manually; and partner-level reporting shows you exactly which T2s are stuck and where. Firm working papers stay in Canadian file storage for clients who expect data residency in Canada.

Related Resources

Frequently Asked Questions

Yes, the template is completely free to download. Fill out the form on this page and you’ll get instant access to the editable file.

The Client & Entity Setup and Corporation-Type Specific Items sections cover CCPCs, non-CCPCs, professional corporations, NPOs, large corporations, and MNEs subject to Global Minimum Tax. Specific schedules and rates flow from the corporation type identified in the first section. For unusual structures, foreign-controlled corporations with complex FAPI, multi-tier holding structures, or M&A-affected returns, customize the template by adding rows specific to the structure.

T2 is the Canadian corporation income tax return; T1 is the personal income tax return. T2s use a different set of schedules (Schedule 1 for book-to-tax reconciliation, GIFI for financial statement data, Schedule 8 for CCA, etc.), different deadlines (6 months after fiscal year-end vs. April 30), and different rate structures (federal corporate rate plus provincial allocation rather than personal marginal brackets). For personal returns, use our T1 personal tax return checklist.

Yes. The Small Business Deduction section walks through CCPC qualification, active business income identification, the federal business limit, the prior-year aggregate investment income reduction, the taxable capital phase-out, and Schedule 23 for associated corporations. It’s built specifically to catch the most common SBD miscalculations before they become reassessments.

Yes, the template is built for team use. Each row has Assignee and Status columns so sections can be split across junior, senior, and partner-level staff. For multi-client visibility, import the checklist into Financial Cents as a project template and attach it to every corporate client’s fiscal year-end automatically.

Open the Google Sheet, make a copy, and edit freely, add rows for firm-specific steps (engagement letter intake, partner review meeting, billing close-out), remove sections that don’t apply to your client base, change the column structure to match your workflow. The template is a starting point, not a fixed process.

No, the template works as a standalone Google Sheet for any T2 engagement. But running a corporate-tax book of more than a handful of clients in spreadsheets gets unmanageable quickly. A practice management system lets you assign the checklist as a recurring project, see every return at a glance, and chase missing client documents on automation. The template plus a system together is what makes corporate tax season survivable.