You’ve spent years building your accounting practice. But here’s a question most firm owners avoid until it’s almost too late: how are you going to exit?

Selling an accounting practice is one of the most significant financial and emotional decisions you’ll ever make. Yet, few owners plan for it with the same intentionality they brought to building it. The result is often a rushed sale, an undervalued firm, and a transition that leaves clients and staff uncertain.

It doesn’t have to go that way. With the right preparation, strategic timing, and a clear roadmap, you can maximize your firm’s value and exit on your own terms.

This guide walks you through every stage, from preparation to post-sale transition, and includes a free checklist to keep you on track. If you are looking at buying an accounting practice, we cover it separately here.

When Is the Right Time to Sell Your Accounting Practice?

There’s no universal answer to this, but the worst time to sell is when you’re forced to. The best exits are planned, not reactive. Here are the most common reasons firm owners decide it’s time.

1. Retirement planning

For most firm owners, a practice sale is the retirement plan. Unlike a salaried employee with a 401(k), your wealth is tied up in the business you’ve built. If you’re within five to ten years of stepping back, now is the time to start thinking about how you convert that asset into retirement income. Starting early gives you room to increase your firm’s value before you go to market, rather than selling at whatever the practice is worth today.

2. Burnout or lifestyle changes

Running an accounting firm is demanding. Tax seasons stack up, client expectations grow, and at some point, the grind outweighs the reward. If you’re feeling that shift, you’re not alone, and it’s a legitimate reason to sell. The key is to act before burnout starts showing up in your numbers. Buyers pay for healthy, well-run practices. A firm that’s been neglected because the owner checked out is a harder sell.

3. Market opportunity

Private equity-backed consolidators are actively acquiring accounting practices, and competition for quality firms is driving valuations up. If your firm is in good shape, the current market may represent a window worth taking seriously. Timing a sale to favorable market conditions, rather than waiting for a personal trigger, can meaningfully impact what you walk away with.

4. Growth plateau

Sometimes a practice reaches a ceiling its current owner can’t push through, whether that’s due to capacity, geography, service mix, or capital. If your firm has strong fundamentals but a limited runway under your leadership, a strategic buyer may be positioned to take it further. For some owners, that’s a reason to hold on and explore other growth strategies for their accounting firm. For others, it’s the right signal to sell to someone with the resources to grow what you’ve built.

5. Health or unexpected circumstances

Illness, a family situation, or a sudden change in circumstances can force the conversation before you’re ready. This is exactly why preparing early matters, even if you have no intention of selling soon. A practice that’s well-documented, properly staffed, and operationally sound is far easier to sell under pressure than one that runs entirely on the owner’s knowledge and relationships.

The Complete Checklist for Selling an Accounting Practice

Selling a practice is a process that unfolds in stages, and each stage has its own set of tasks that can make or break your outcome.

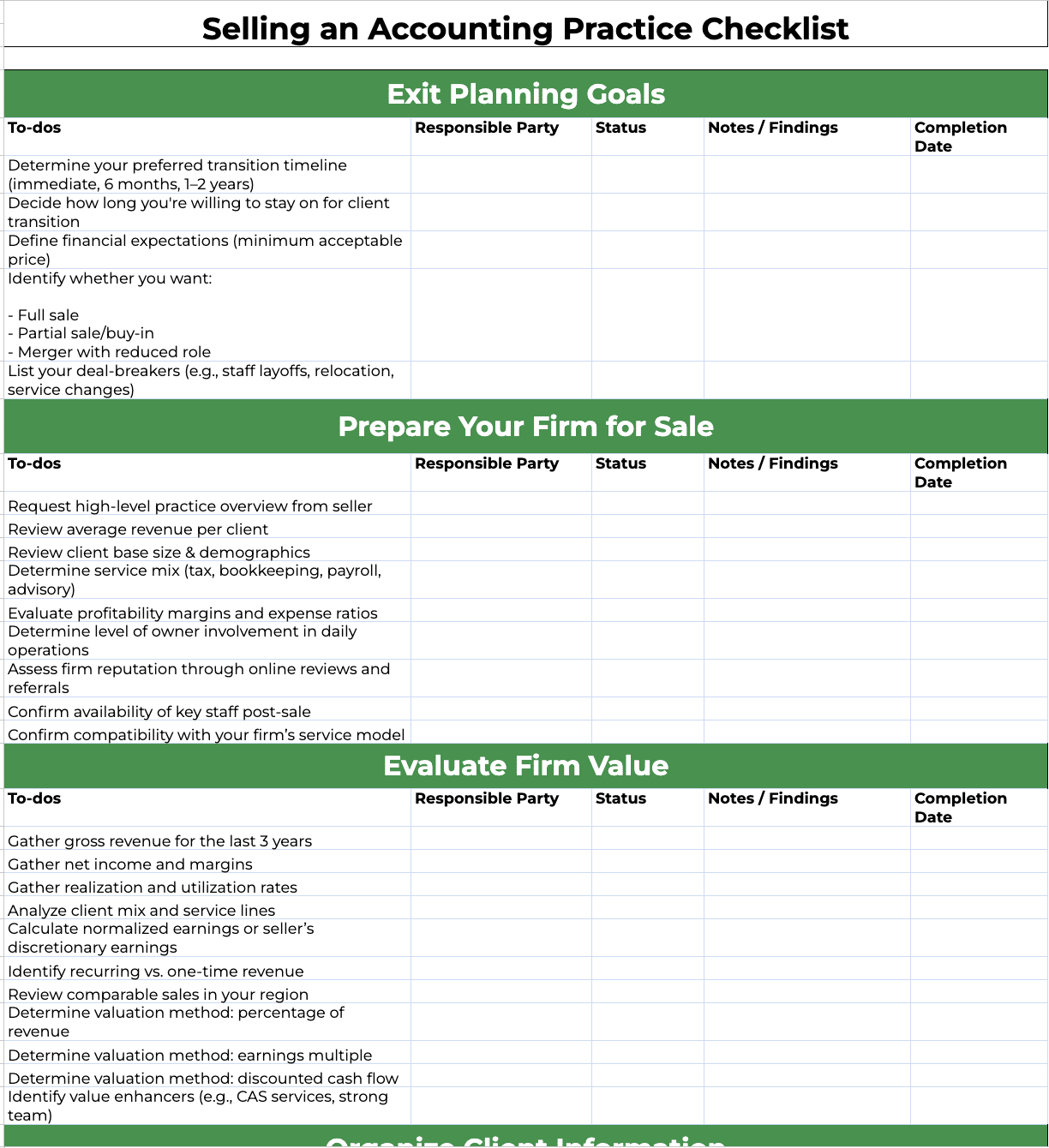

1. Plan Your Exit

Before anything else, get clear on your goals. What does a successful sale look like for you? How involved do you want to be post-sale? What’s your ideal timeline? What’s the minimum number you’d accept?

These questions determine the type of buyer you should target, the deal structure you’ll accept, and how aggressively you need to prepare.

A full sale is the cleanest break, but it’s not the only option. Some owners prefer a partial sale or buy-in arrangement, while others consider a merger that allows them to step back gradually while staying involved in a reduced capacity. Each path attracts a different type of buyer and requires a different approach.

You should also define your deal-breakers upfront. If staff layoffs, client service changes, or relocation are non-starters for you, document that before you start any buyer conversations.

2. Prepare Your Firm for Sale

Think of this as getting your house ready before listing it. The goal is to make your practice as attractive and easy to evaluate as possible.

That means cleaning up your financials, documenting your processes, addressing any operational gaps, and reducing owner dependency wherever you can.

Take stock of your service mix, too. Be clear on what percentage of your revenue comes from tax, bookkeeping, payroll, and advisory work. Buyers evaluate this early because it shapes how they’ll integrate your firm into their own operations. A practice with a strong advisory services, for example, is often viewed more favorably than one that’s heavily compliance-dependent.

Also, assess your firm’s reputation and marketing presence. Check your online reviews, think about your referral volume, and be honest about how your firm is perceived in your local market. Buyers do this research anyway. Knowing where you stand gives you a chance to address any gaps before they become negotiating points.

3. Evaluate Firm Value

Understanding what your practice is worth requires looking at two things together: your financials and your client base.

On the financial side, start by pulling your gross revenue, net income, and profit margins for the last three years. Go deeper than the top-line numbers in your reporting. Buyers will want to see your realization and utilization rates, your recurring versus one-time revenue split, and your normalized earnings or seller’s discretionary earnings, which strips out owner-specific expenses to show what the business actually generates.

Research comparable sales in your region to understand where your firm sits relative to the local market. Going in blind on price is one of the most common mistakes sellers make.

4. Organize Client Information

On the client side, build a detailed client list with revenue broken down by client. Identify the high-value relationships that will matter most to a buyer, and flag any clients who may be at risk of leaving during a transition.

Document client contact information, service history, preferences, and any cross-selling opportunities that exist within your current base. Workflow software for accounting firms makes it significantly easier to pull this information together in a format buyers can actually evaluate.

5. Prepare Staff and Operations

Start by creating an organizational chart that clearly maps out roles and responsibilities. Review and update employment agreements while you’re at it; outdated or informal arrangements create unnecessary complications during due diligence. Document staff productivity and utilization metrics too, as buyers will want to see how efficiently your team operates.

Identify key staff and think honestly about retention. Will they stay post-sale? Some sellers include stay bonuses in the deal structure to give buyers confidence that critical people won’t walk out the door.

Operationally, document your workflows. If your accounting workflow management process exists only in people’s heads, write it down. The buyer should be able to pick up that documentation and understand how work moves through your firm without asking you for every detail.

Finally, verify that your payroll, HR records, and benefits information are accurate and up to date.

6. Legal and Compliance Readiness

This stage is about making sure everything is in order before a buyer starts asking questions.

Start with your compliance fundamentals. Confirm that your CPA licensing is current and in good standing, and verify your IRS e-file compliance status.

Review your entity documentation and operating agreements, particularly if your practice is structured as a partnership. Check for any provisions that affect a sale and address them before you’re in active negotiations. Also, surface any existing legal or financial liabilities upfront.

On the insurance side, review your Error and Omissions (E&O) coverage and claims history, not just whether the policy is active. Gather your vendor contracts, lease agreements, loan documents, and software license agreements, including renewal dates. Check all of these for change-of-ownership clauses that could complicate a transfer.

7. Improve Practice Marketability

This is about making your firm as attractive as possible before you start buyer conversations. Some of these are quick fixes. Others take time, which is why starting early matters.

Address any profitability issues and resolve overdue work-in-progress and old accounts receivable. Buyers look at these as signs of poor financial discipline, and cleaning them up before going to market removes an easy objection. Reduce owner dependency in client relationships wherever you can. The more clients are tied to your firm rather than to you personally, the lower the transition risk a buyer has to price in.

Update your branding, website, and marketing materials. It sounds superficial, but a firm that looks professionally run signals to buyers that the business has been well managed. Improve your client communication templates too, and strengthen your internal documentation and controls. These details collectively paint a picture of a firm that operates with consistency and care.

If you want a structured approach to getting there, check out the 5-Day Email Course: Build a Buyer-Ready Practice with Adam Shay.

8. Create Your Seller’s Information Package

Your Seller’s Information Package, sometimes called a Confidential Information Memorandum, is the document you share with serious buyers. It needs to be thorough, well-organized, and professional.

At a minimum, it should include an executive summary of your firm, a three-year financial summary, and your asking price with valuation rationale.

Add a team overview that outlines your staff structure, a client demographic analysis that goes beyond a simple client list, and a breakdown of your accounting software stack and systems so buyers understand what tools the firm runs on. Include your workflow and process documentation, lease details, and a draft transition plan outline that gives buyers a sense of how a handover would work in practice.

This document sets the tone for how buyers perceive you as a seller.

9. Find and Vet Buyers

Start by deciding whether you’ll use a broker or pursue a private sale. Both are viable paths, but the right choice depends on how much of the process you want to manage yourself and how broad a buyer pool you need access to.

Your options include existing partners, internal succession candidates, CPA firm networks, practice brokers, industry marketplaces, and strategic acquirers. Each channel attracts a different type of buyer, so align your choice with the kind of exit you’re looking for.

Before sharing any sensitive information, have prospects sign an NDA. From there, review each buyer’s financial capability to confirm they can actually close. Validate their CPA licensing and experience, evaluate cultural fit, and take time to understand their long-term goals for the practice. The right buyer isn’t always the highest bidder.

10. Negotiate the LOI

A Letter of Intent outlines the basic terms of the deal before you move into formal agreements. Agree on your purchase price or range and settle on a payment structure, whether that’s cash, seller financing, an earnout, or a hybrid arrangement. Define the length of the transition period, establish non-compete and non-solicit clauses, and clarify exactly which assets and liabilities are being transferred.

11. Final Due Diligence

At this stage, the buyer will want to verify everything you’ve represented about your practice. Be prepared to provide detailed financial records with full backup for revenue and expenses, sample client files, staff performance summaries, a software access overview, lease and vendor agreements, legal compliance confirmations, E&O insurance confirmations, and tax filings for your entity. The more organized you are going in, the faster this stage moves.

12. Execute the Purchase Agreement

Once due diligence is complete, it’s time to formalize the deal. Sign the final purchase and sale agreement, confirm the payment schedule and escrow arrangements, and complete any licensing and registration updates required. Finalize staff transition agreements, coordinate with your attorneys and accountants, and update your insurance policies accordingly.

13. Transition Execution

Start by notifying your staff, then your clients. Introduce the buyer to your top clients personally and provide them with training and system access so they can hit the ground running. Complete data migration, oversee the workflow and engagement handoff, and support the buyer throughout the transition period. Your involvement during this stage directly affects how smoothly clients transfer and how well the practice holds together under new ownership.

14. Post-Sale Wrap-Up

Once the transition is complete, tie up the remaining loose ends. Finalize the payout of any outstanding accounts receivable and monitor any seller financing or earnout arrangements still in play. Update your personal licensing status and remove your access from all firm systems. Transfer ownership of the domain, website, and email accounts to the buyer. Then conduct a final meeting with the buyer to close out the process formally and confirm everything has been handed over as agreed.

Free Checklist Template for Selling an Accounting Practice

Every stage covered in this guide maps to a specific set of tasks you need to complete before, during, and after your sale. To make it easier to track your progress, we’ve put together a free checklist template you can use from day one.

Selling an Accounting Practice Checklist

Common Mistakes When Selling an Accounting Practice

Waiting too long to prepare

By the time most owners are ready to sell, there’s no time left to address valuation gaps or clean up operations. The earlier you start, the more options you have.

Overvaluing the firm

Emotional attachment is understandable, but buyers look at the numbers. Pricing above what your financials justify shrinks your buyer pool and stalls deals. Get an independent valuation first.

Failing to document processes

If your operations live in your head, buyers will price that risk into their offer. Documented workflows signal that the practice can function without you.

Poor client communication

Clients who hear about a sale from someone other than you lose trust fast. Plan your communication strategy early and control the narrative.

Ignoring staff retention

If key staff leave before or during the transition, it raises red flags and can affect your earnout payout. Have honest conversations early and consider retention incentives.

Choosing a buyer solely on price

The highest offer isn’t always the best deal. Evaluate financial capability, operational fit, and culture alongside the number.

Failing to plan the transition

Disengaging too quickly after closing is one of the fastest ways to lose clients post-sale. Honor your transition timeline and stay engaged.

How Strong Systems Increase the Value of Your Practice

When a buyer evaluates your firm, they’re assessing risk. The firms that command the strongest valuations are the ones that can demonstrate they’ll hold together once the current owner leaves. Your systems are how you prove that.

Documented workflows

When your processes are written down and consistently followed, it signals that the business can be handed off without everything falling apart. Firms that have invested in accounting practice management software before going to market move through due diligence faster and with fewer surprises.

Centralized client information

Disorganized client data is a transition risk in a buyer’s eyes. A centralized system that gives a clear picture of every client relationship tells a very different story.

Standardized service delivery

Consistency reduces dependency on specific individuals and makes the firm easier to scale. Buyers know what they’re getting. That certainty has real value.

Clear task ownership

Buyers want to see a well-managed firm with defined roles and clear accountability. If answering “who owns what” requires a conversation with you, that’s a risk buyers will price in.

Operational transparency

Real-time visibility into what your team is working on reduces the unknown. Buyers pay more for firms that leave less to the imagination.

Financial Cents practice management software is built to help you build exactly these systems. Getting your practice onto a solid practice management platform before you go to market is one of the highest-return investments you can make.

Conclusion

The firm owners who exit well are the ones who started preparing long before they were ready to sell. They documented their processes, organized their client data, and built a practice that could stand on its own. When the time came, they had options.

The ones who struggled waited too long and had to accept whatever was on the table.

Use the checklist in this guide as your starting point. Work through each stage, address the gaps, and give yourself enough runway to make meaningful improvements before you go to market. The work you do now directly shapes what you’ll walk away with later.

Financial Cents is an all-in-one accounting practice management software that centralizes your client information, standardizes your workflows, clarifies task ownership, and gives you real-time visibility across your firm. Everything a buyer wants to see, and everything you need to manage your practice effectively in the meantime.

Use Financial Cents to manage your accounting firm

Frequently Asked Questions

Most practices sell for between 0.9x and 1.3x gross recurring revenue, though this can stretch higher for firms with strong profitability, low client concentration, and consistent growth. An independent valuation from someone familiar with the accounting industry will give you the most accurate picture.

Most sales take between six months and two years from going to market to closing. Well-organized firms priced realistically move faster. Complicated financials or operational gaps slow things down.

A specialist broker brings a vetted buyer pool, manages confidentiality, and guides negotiations, typically for 10 to 12 percent of the sale price. If you already have a likely buyer or are comfortable running the process yourself, you may not need one. For most first-time sellers, a good broker pays for themselves.

The most common benchmark is one times gross recurring revenue, though advisory-heavy firms with strong margins can command higher multiples. Compliance-focused or owner-dependent practices typically land at the lower end. Buyers are increasingly looking at profitability, not just revenue.

Yes, but it limits your buyer pool. Without staff, the business is more dependent on you personally, which buyers see as a transition risk. Strong client retention, documented processes, and recurring revenue help offset that concern.