Every firm reaches the point where a client relationship stops working. And still, sending a termination letter feels uncomfortable, like you’re the one doing something wrong.

That discomfort is normal. Most accountants avoid the conversation until they can’t anymore, and the bad-fit client stays on the books, draining your team’s energy and your firm’s margins.

A professional disengagement letter is the kindest and safest way to end a relationship. It gives the client a clear, effective date, a clean handover of records, and enough time to find new representation. It gives your firm a documented, liability-aware close. Done right, it’s not confrontational.

This guide covers when to terminate, the eight elements every letter needs, what to do after you send, and the legal considerations specific to CPAs.

What Is a Client Termination Letter for Accountants?

A client termination letter is a formal written notice ending the professional engagement between your firm and a client. It states the effective date, the status of outstanding work, and how client records will be returned or transferred.

The AICPA calls it a disengagement letter. Some accounting firms also use client termination letter, letter to terminate accounting services, or letter of disengagement interchangeably; same document, same function. The written record is what your malpractice insurer, state board, or legal counsel will ask for later.

The cleanest terminations start with a strong accounting engagement letter. When the engagement letter is vague or nonexistent, termination gets messier.

When Should an Accounting Firm Terminate a Client?

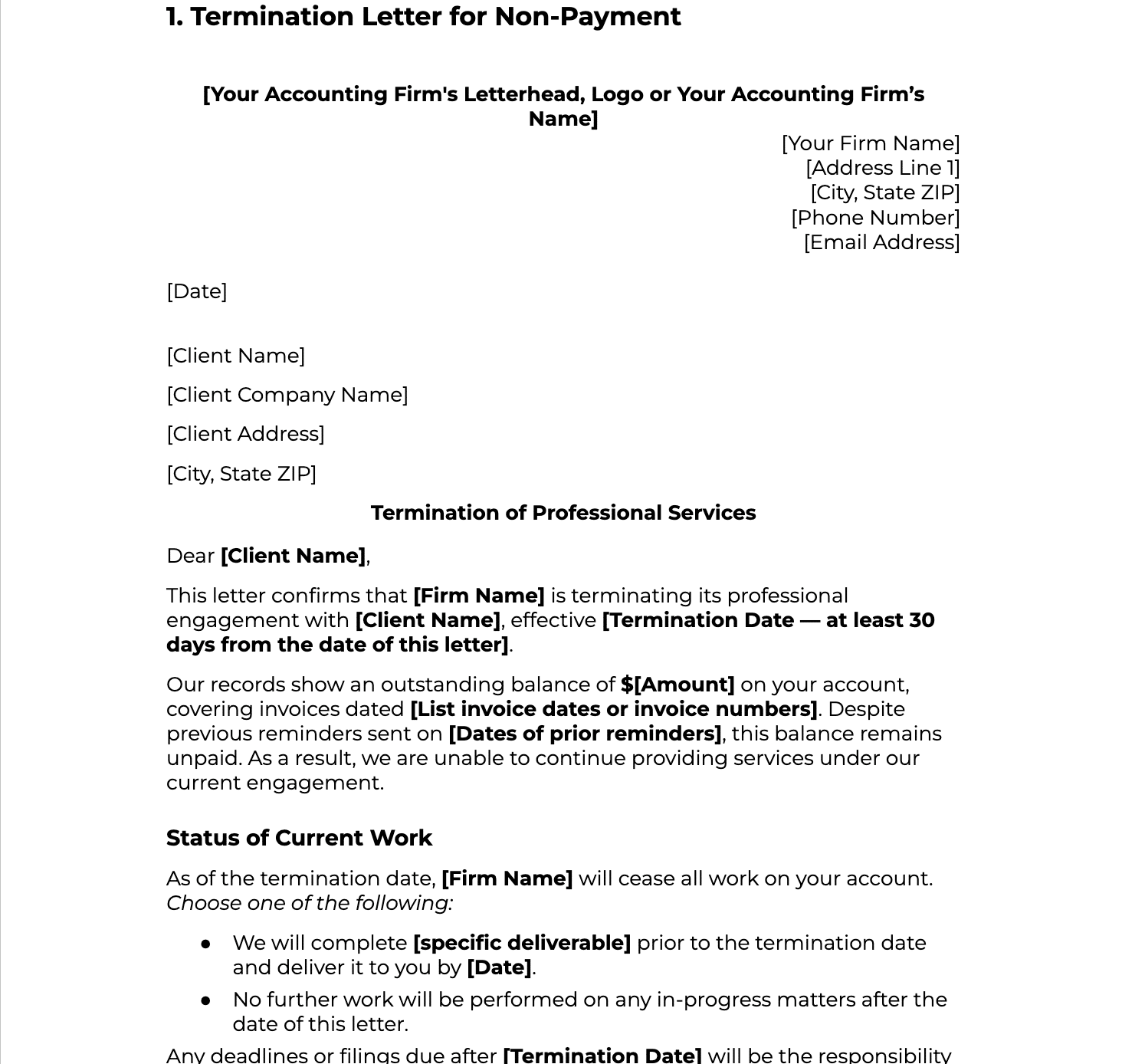

a. Non-payment or chronic late payment

The most common trigger. A client who consistently pays late forces your firm to carry the cost of their work, distorts cash flow, and tells your team that collection is optional.

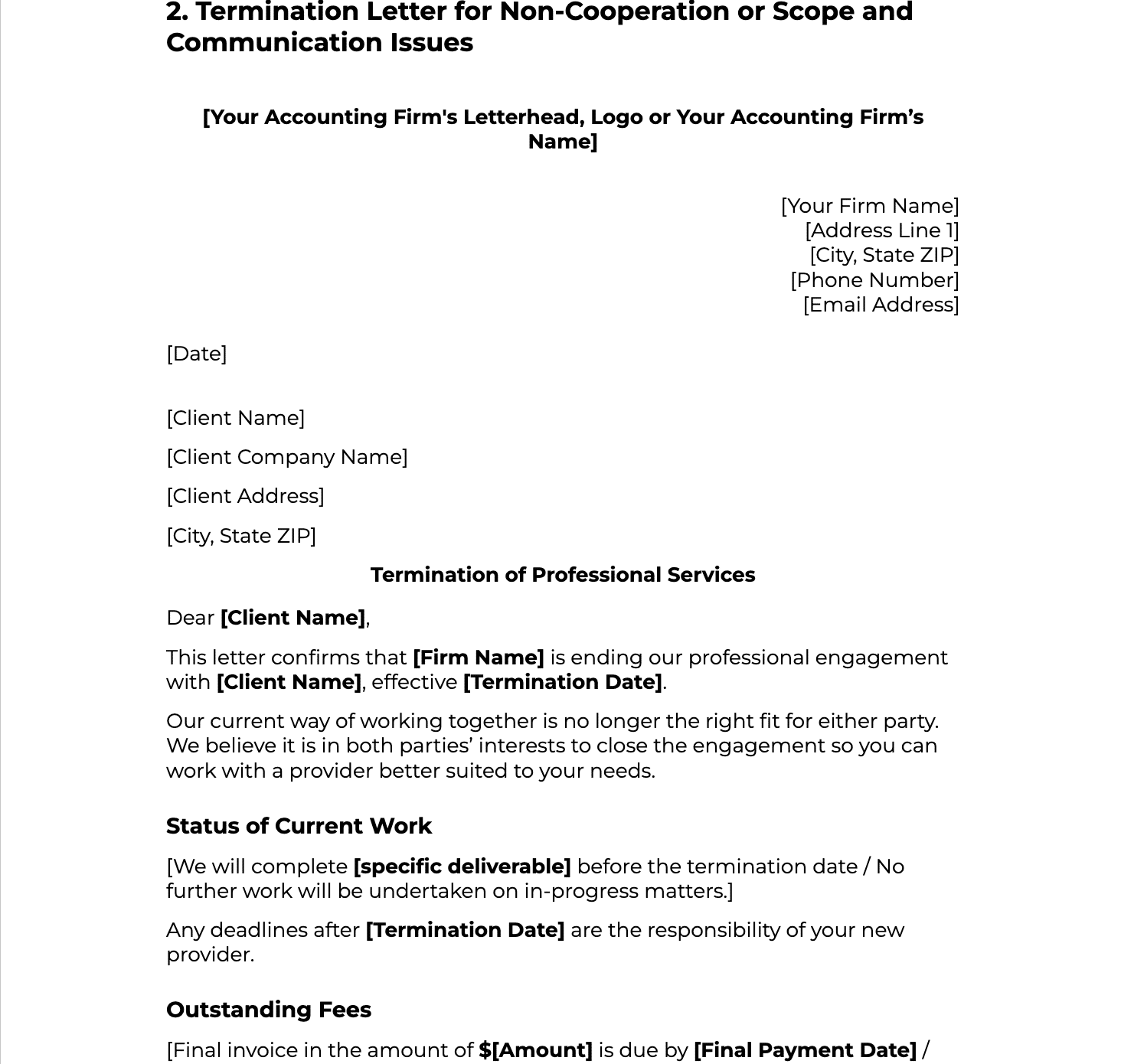

b . Failure to provide information or documents

When a client repeatedly misses deadlines, ghosts your requests, or sends information in pieces that force your team to redo work, the engagement stops being profitable. Chasing documents becomes a bigger job than the engagement itself.

c. Scope creep and boundary violations

Scope creep starts small, a quick question turns into a full advisory conversation, a one-off request becomes a monthly expectation. Before long, the client is consuming two or three times the work you priced for.

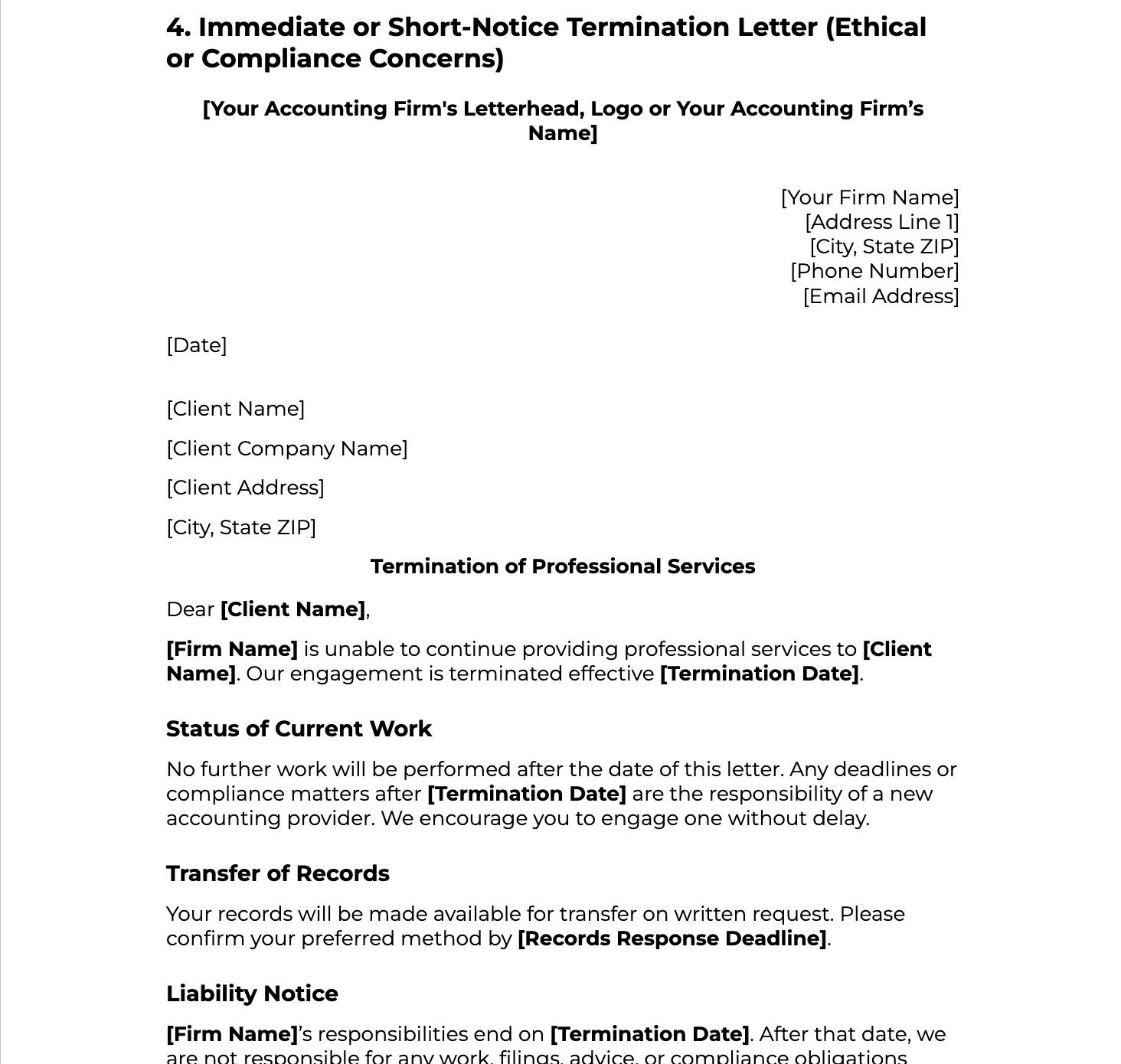

d. Ethical concerns or compliance risks

Sometimes a client asks you to do something you can’t do, misrepresent figures, omit income, ignore a compliance issue. When professional standards can no longer be met, termination isn’t optional.

For ethical terminations, your letter should not state the concern, or any reason. AICPA guidance is explicit on this. Neutral language like “our firm will no longer provide services to you” is sufficient. Consult your state CPA association, liability insurer, and legal counsel first. The AICPA’s PCPS Client Disengagement and Termination Letter is the authoritative reference on this.

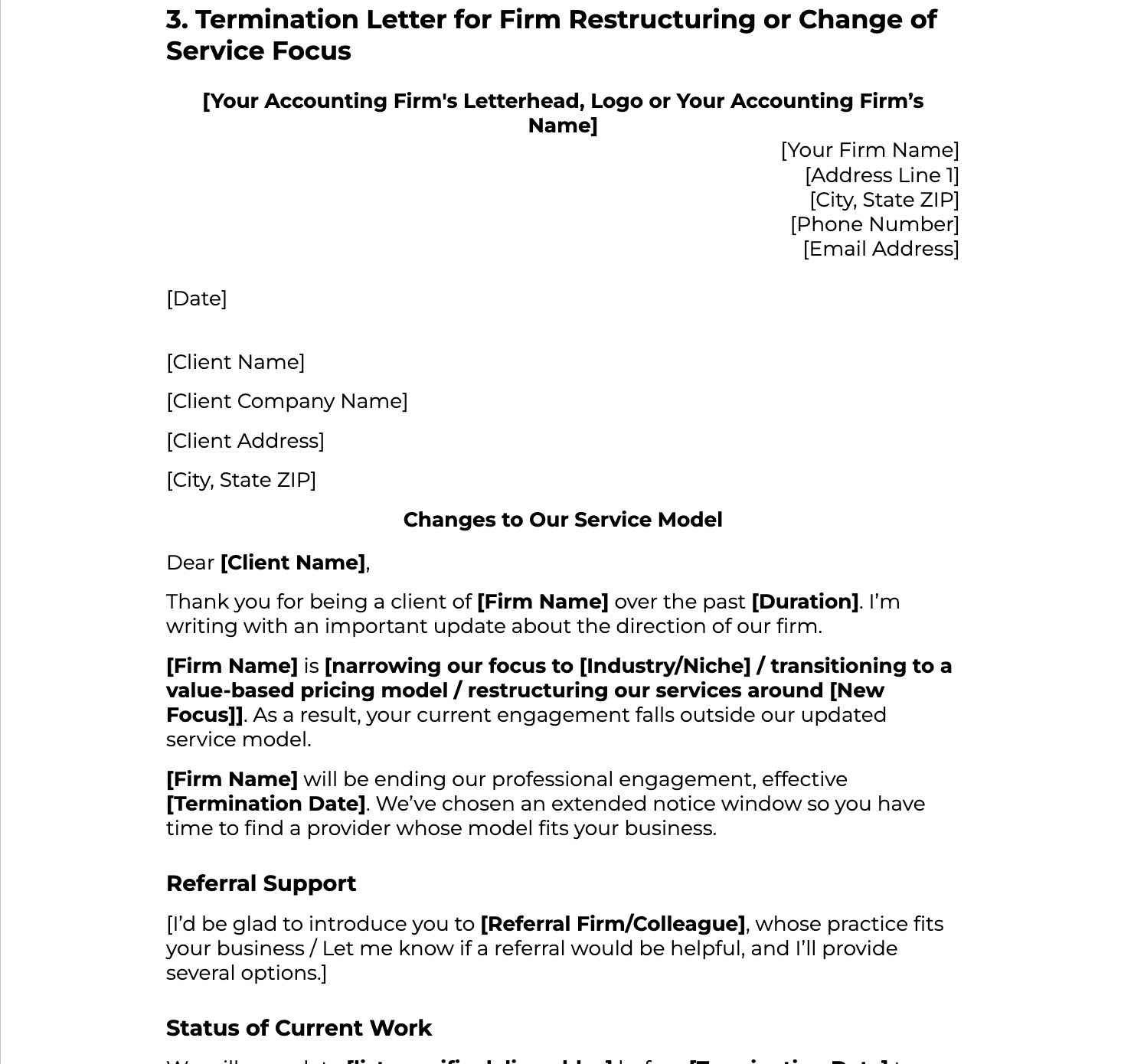

e. Firm restructuring or niche change

As firms niche down, move upmarket, or transition to value pricing, some long-standing clients stop fitting the new direction. These aren’t bad clients, just no longer the right ones for the firm you’re becoming.

Firms mid-transition, niching down or rethinking how to price bookkeeping services should expect these conversations as a matter of course.

f. Client behaviour affecting your team

A single difficult client can quietly damage your firm from the inside. Rudeness, boundary-pushing, or a pattern of blame when mistakes happen erode morale faster than most firm owners realise. If you’re losing good people or shielding your team from one client, the math is already clear.

What to Include in a Client Termination Letter

A strong termination letter fits on a single page. Every element earns its place, closing the engagement cleanly, protecting your firm legally, or giving the client what they need to move on.

I. Header

Your firm’s letterhead, the date, and the client’s full legal name and mailing address. For business clients, include the business name exactly as it appears on your engagement letter.

II. A clear termination statement and effective date

The most important line. Something like: “This letter confirms that [Firm Name] is terminating its professional engagement with [Client Name], effective [Date].” Give at least 30 days’ notice where possible. Shorter notice fits only ethical concerns or serious non-cooperation.

III. A brief, professional reason

A short, neutral reason adds clarity. Non-payment? Reference the outstanding balance. Non-cooperation? Reference the repeated delays. Firm direction change? Reference the shift in your service model. Ethical termination? The rule flips, do not state a reason.

IV. Status of current work

Be explicit about where in-progress work stands on the termination date. Will you complete current deliverables? Will the client receive a partial report? Will filings be handed off? Ambiguity here is where disputes start.

V. Outstanding fees

Address any balances owed or credits due back. State the amount, the due date, and how collection will be handled if the balance isn’t settled. For prepaid work that won’t be completed, explain how and when the refund will be issued.

VI. Records transfer

Tell the client which records you’ll return or transfer, how they can collect them, and the deadline to respond. Note your retention period. It typically varies by state.

VII. A liability disclaimer

A short paragraph confirming your firm’s responsibilities ends on the termination date, that you aren’t responsible for work or filings after that, and that the client should engage a new accountant promptly. The single most important clause for liability protection.

VIII. A professional close

Thank the client where appropriate, offer reasonable help with transition, and sign with the name and title of the partner sending the letter. A warm close is your last impression; it often determines whether the client speaks well of your firm afterwards.

Download the free client termination letter template (available in Word & Google docs format) to get every element above in a fill-in-the-blank format, with variants for non-payment, non-cooperation, firm restructuring, and short-notice ethical terminations.

Download the Accounting Client Termination Letter SamplesAccounting Client Termination Letter Samples [Word & Google Docs]

1. Non-Payment

2. Non-Cooperation / Scope and Communication Issues

3. Firm Restructuring or Change of Service Focus

4. Immediate or Short-Notice Termination (Ethical or Compliance Concerns)

What to Do After Sending the Termination Letter?

Sending the letter is the midpoint, not the finish line. The hours after it goes out are where firms either close the engagement cleanly or leave loose ends that surface later as disputes.

Document the sending

Keep proof that the letter was sent and received, certified mail return receipt, email read receipts, or the client portal log. This is what you’ll point to if the client later claims they never received notice.

Complete any work you committed to finishing

Whatever the letter promised (current month’s bookkeeping, a final tax return, a specific deliverable), complete it to your normal standard. Cutting corners on committed work is how clean terminations turn into malpractice complaints. Delivering consistent client deliverables matters as much at the end as at the start.

Collect and transfer records

Compile the client’s records and make them available through the method they confirmed, source documents, working papers you’re obligated to return under state rules, and deliverables that belong to them. Confirm your retention copies are stored securely.

Settle outstanding fees

Issue final invoices promptly and follow your standard collections process. Unresolved fees are the most common source of post-termination disputes, every week that passes makes them harder to collect.

Update your practice management system

Close out the client record so the engagement stops generating activity; archive the client, deactivate recurring tasks, and remove them from active reporting. Financial Cents practice management system lets you archive clients in a single click; the record stays accessible but disappears from your active workflow. The best accounting practice management software handles this lifecycle step cleanly so terminated clients don’t resurface by accident.

Brief your team

Everyone who worked on the account needs to know the engagement has ended, what was communicated, and what to do if the client calls. A short internal memo prevents an off-script conversation from undoing the tone you worked to establish in the letter.

Legal Considerations for CPAs Terminating Client Relationships

CPAs operate under a specific professional liability framework, and how you handle a termination affects your license, your insurance, and your exposure to claims.

Never abandon a client mid-engagement

The biggest liability risk in a poorly executed termination. If you terminate during active tax season, mid-audit, or with a filing deadline bearing down and the client misses it, you can be held professionally responsible, even if the client caused the delay. If timing is unavoidable, your letter must explicitly state what work will and won’t be completed before the effective date.

State CPA associations have specific requirements

Your state board and state CPA society may have rules on records retention, notice periods, and disengagement procedures that differ from AICPA guidance. These are licensing requirements, not suggestions. Verify the minimum notice period, state rules on returning records regardless of unpaid fees, and any required disclosures before finalising the letter.

Do not admit liability or wrongdoing in writing

Review every sentence through one question: could this be read as an admission? Apologies, explanations of internal mistakes, and references to past errors do not belong in a termination letter. An apologetic letter can be introduced as evidence in a claim the client hasn’t even filed yet.

Seek counsel during an active examination

If your client is under IRS examination, a state tax audit, or any regulatory investigation, consult legal counsel before sending. Terminations during active proceedings often trigger disclosure obligations that aren’t obvious from the engagement letter alone.

Verbal terminations are not enough

A phone call or a casual “we’re going to part ways” does not close an engagement for liability purposes. You need a dated, written document; it’s the first thing your insurer will ask for. The dos and don’ts of engagement letters is worth a read; most termination disputes trace back to ambiguity in the original engagement.

This is general guidance, not legal advice. Ethical terminations, active litigation, or clients in regulated industries warrant a conversation with qualified counsel and your liability insurer before you send anything.

Conclusion

Ending a client relationship is uncomfortable. It’s also, at some point, unavoidable; every firm that grows, niches, or protects its margins will eventually need to let a client go. The firms that do it well don’t avoid the conversation. They handle it on paper.

The cleanest way to avoid difficult terminations isn’t to avoid the conversation, it’s to build a firm where fewer of them are necessary. That means sharp engagement letters at the start of every relationship, clear scope and pricing, and a practice management system that keeps every engagement visible and accountable from day one.

That last piece is where Financial Cents comes in. Financial Cents is practice management software for accounting firms that brings your entire client relationship, workflow, communication, document requests, deadlines, billing, and records into one system. Firms use it to catch the early warning signs of a bad-fit engagement long before it gets to a termination letter, and to archive cleanly when a termination is the right call.

Download the free template to get started, and start a free trial of Financial Cents to manage the full client lifecycle, so the next time a relationship isn’t working, you’ll have both the letter and the documented history to end it cleanly.