Instead of building a firm from scratch, many accounting professionals choose to buy an existing practice. It’s one of the fastest ways to grow revenue because you acquire an established client base and often a trained team.

However, buying an accounting practice carries real risk. Many buyers focus on revenue and valuation and underestimate what it takes to combine two firms operationally. Differences in workflows, technology, client communication standards, and management style can create problems during the transition.

In a McKinsey survey, 44% of M&A leaders cited a lack of cultural fit and friction between the acquiring and target companies as the top reasons integrations fail. This shows that execution during integration determines whether an acquisition succeeds.

You need a clear plan to integrate systems, standardize processes, retain clients, and support staff through the transition. If you ignore these areas, you might lose staff, clients, and revenue soon after closing the deal.

We share everything you need to know about buying an accounting practice in this guide. You’ll also get a free checklist to help you stay organized and make a confident decision.

Why Buy an Accounting Practice Instead of Growing Organically?

Buying a practice isn’t the right move for everyone. But for the right firm, it can accelerate growth in ways organic expansion simply cannot.

Immediate Revenue and Cash Flow

One of the biggest advantages of buying a practice is immediate revenue. When you acquire a firm, you take over active engagements and existing recurring fees from day one. That means you’re not investing months or years in marketing campaigns, client pitches, or sales cycles to generate the same revenue.

Having a reliable revenue stream improves cash flow and supports future growth.

Established Client Base

Winning new clients is expensive and time-intensive. In professional services, trust drives buying decisions, and trust takes time to build.

Instead of starting from zero, you begin with a base of engaged clients who already trust the practice and value the services being delivered.

This doesn’t guarantee retention, but it does eliminate the long ramp-up period required to build credibility in a new market or service line.

Trained Staff and Existing Processes

Hiring and training staff and building systems that work take time and experience. By buying a practice with an experienced team in place, you save significant time and cost associated with recruiting, onboarding, and training hires.

These staff also bring institutional knowledge about the firm’s service, client expectations, internal workflows, and technology.

In many cases, staff retention directly supports client retention. Clients are more likely to stay when familiar team members remain involved in their work.

Faster Growth With Less Marketing Effort

Organic firm growth relies heavily on marketing, networking, thought leadership, referrals, content creation, and other demand-generation activities. Some firms invest hundreds of hours each month in content, SEO, and relationship-building to sustain a growth pipeline.

An acquisition reduces the reliance on marketing to drive growth because you’re purchasing existing demand. The acquired firm already has clients, referral sources, and market presence. While you may still invest in marketing post-acquisition, your efforts shift from building baseline revenue to expanding and optimizing what you’ve acquired.

You also create cross-selling opportunities. Clients of the acquired firm may now access additional services you already offer, increasing average revenue per client without new acquisition costs.

Exit Opportunities for Retiring Owners

More practices are for sale because owners are planning their exit. According to AICPA’s PCPS succession planning data, 44% of solo practitioners plan to retire soon, which is one reason acquisitions have become a common growth path.

For retiring owners, selling to another firm provides continuity for clients and staff. For buyers, it creates opportunities to acquire established revenue from motivated sellers who are willing to support a structured transition.

Succession-driven deals often include seller involvement during the handoff period, which can improve client retention and make integration smoother.

Types of Accounting Practices You Can Buy

When you’re looking to buy an accounting practice, you need to understand what kind of firm you’re actually acquiring. Different practice models come with different revenue stability, staffing needs, operational complexity, and retention risk. The better you understand the model, the easier it is to assess fit and value.

Solo Practitioner Practices

Solo accounting practitioners are small practices run by one accountant, often with one or two support staff. These firms typically focus on compliance services like tax preparation, year-end filings, and basic bookkeeping. Because they’re small, their pricing and service model is usually straightforward, and client relationships tend to be personal and direct.

Small Bookkeeping Firms

Bookkeeping firms specialize in maintaining financial records for businesses. They track transactions, reconcile accounts, manage accounts payable/receivable, and prepare basic financial reports.

See this accounting firm organizational chart guide for the type of structure and roles to expect based on the fimr size.

Niche Firms

Some firms specialize in a specific service line rather than offering a full-service model. These can include tax-only firms, Client Accounting Services (CAS) firms, bookkeeping-only practices, or audit-focused firms. Niche firms are useful acquisition targets if you want to expand a specific offering.

Local vs Remote Firms

Local firms have a physical presence in a specific community or region. They typically focus on clients in that market and often provide face-to-face service. These firms might have deep local knowledge of tax laws, business climates, and regulatory environments, which can be a differentiator for clients who value personal interaction.

Remote accounting firms operate virtually, serving clients anywhere through online communication, cloud accounting tools, and digital workflows. These firms can scale more easily across regions and often appeal to clients comfortable with technology.

You may be interested:

18 Practical Strategies for Managing an Accounting Firm

How Accounting Firms Are Valued

To value a firm, buyers look at several financial and operational metrics to arrive at a fair price. Here are the key valuation concepts you need to understand.

Revenue Multiples

One of the most common valuation methods in smaller accounting practice transactions is a revenue multiple. This approach multiplies annual gross revenue by a market-based factor and gives buyers a quick estimate of market value relative to other deals.

Firms with a high percentage of recurring revenue (like monthly bookkeeping, payroll, or ongoing CAS engagements) tend to command higher multiples because those fees are predictable and less volatile.

Revenue tied to one-time projects, irregular advisory work, or seasonal spikes is typically viewed as less stable and may justify a lower multiple.

EBITDA or Cash-Flow-Based Valuations

Another way to value a firm is based on profitability, often using Earnings Before Interest, Taxes, Depreciation, and Amortization (EBITDA) or a cash-flow measure.

EBITDA reflects the firm’s operational earnings before financing and accounting adjustments. For many mid-sized firms, buyers use EBITDA multiples to understand how efficiently the firm converts revenue into profit.

This approach is especially useful when two firms generate similar revenue but very different profit margins. A firm with stronger margins and disciplined cost management will typically justify a higher valuation than a firm with high overhead and low profitability because it converts more revenue into earnings.

Smaller, owner-dependent firms may also be valued using Seller’s Discretionary Earnings (SDE), which includes owner compensation and discretionary expenses. This method can give a realistic picture of what a new owner can expect in cash flow after the previous owner leaves.

Client Retention Risk

Buyers pay close attention to client retention because the long-term value of the firm depends on how many clients continue after the sale. If most of the revenue comes from clients who stay year after year, the firm is worth more. If the client base churns frequently, adjust valuation downward to reflect that risk.

Owner Dependency

Firms where the owner does most of the technical work or maintains all client relationships, and makes key decisions alone are inherently riskier. Buyers value independence and systems over owner reliance because if clients chose the firms solely because of the owner, they may leave after the sale.

Staff and Systems Maturity

Strong operations make a firm more valuable. Well-run firms with stable teams and documented systems signal lower operational risk and often command higher valuations. Buyers interpret this as a proxy for future performance and retention.

In contrast, firms with unclear responsibilities, undocumented processes, and fragmented systems may require significant restructuring after acquisition. That integration effort represents cost and risk, which should be reflected in deal terms.

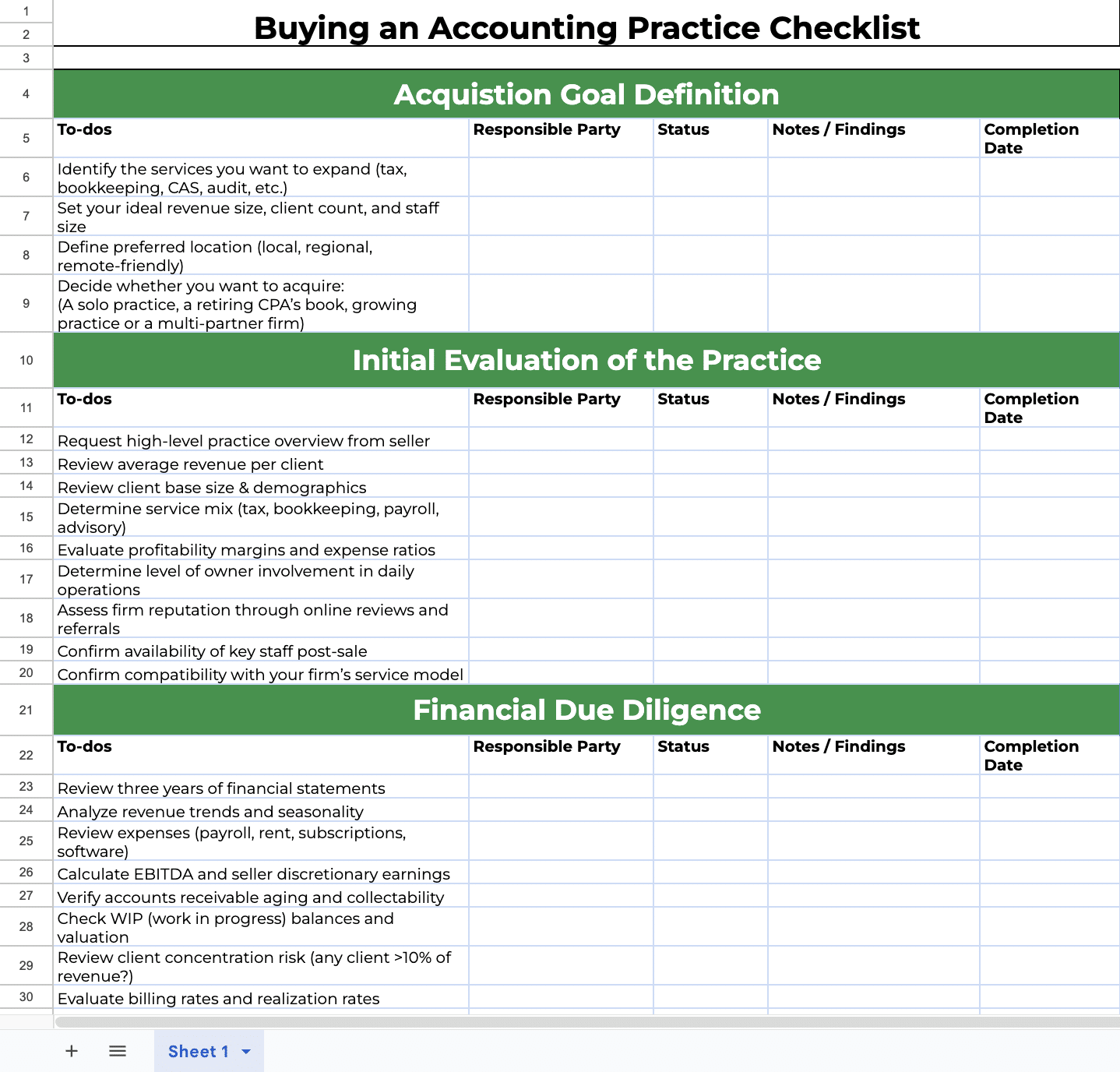

Checklist for Buying An Accounting Practice

Follow the steps in this checklist diligently when buying an accounting practice to avoid making a mistake. You can also download the full checklist below (it is available in excel and Google sheets format)

Step 1: Define Your Acquisition Goal

Before reviewing any firm for sale, clarify exactly what you want to achieve.

Are you trying to add recurring monthly bookkeeping revenue? Expand into advisory? Enter a new geographic market? Your objective determines the type of firm you pursue, the revenue size you target, and the level of operational complexity you are prepared to absorb.

Write down your criteria. Define the minimum revenue range, client count, staff size, service mix, preferred location, and type of practice (solo, multi-partner, etc). When you then see an opportunity, evaluate it against this framework instead of getting distracted by attractive revenue numbers that don’t align with your strategy.

Step 2: Perform an Initial Evaluation

Once you identify a firm that matches your goals, conduct an initial review before committing to deeper diligence.

Request a high-level practice overview from the seller, a breakdown of revenue by client, service mix, profitability margins, level of owner involvement in daily operations, firm reputation, and compatibility with your firm’s service model.

If the practice doesn’t pass this evaluation, walk away. Early exit saves time and legal costs.

Step 3: Financial Due Diligence

If the opportunity passes your initial screening, proceed to detailed financial analysis.

Start by reviewing the last three years of financial statements. Analyze revenue trends, expenses, calculate EBITDA and seller discretionary earnings, and verify accounts receivable aging and collectability.

Also, check WIP (work in progress) balances and valuation, client concentration risk (does any client exceed 10% of revenue?), billing rates and realization rates, and tax returns for the firm entity (if available).

Step 4: Operational Due Diligence

Strong financials do not guarantee a smooth transition. You need to understand how the practice actually runs.

Review workflows for recurring services such as bookkeeping, close cycles, tax preparation processes, and payroll delivery. Are there documented procedures?

Assess the technology stack. Identify whether client documents are centralized, how communication is managed, and whether there is a formal accounting practice management system in place. Check cybersecurity and data security protocols to ensure sensitive information is protected.

Evaluate staff roles, productivity, and utilization rates, and determine staff turnover rate. You might also need to inspect the physical office (if included in the sale).

Step 5: Review the Client Base

The real asset in an accounting practice acquisition is the client base. Study it carefully.

Analyze the client industries and service types, client retention rate over the last three years, recurring revenue percentage, and client concentration risk. If >10-15% of revenue comes from one client, it’s risky.

Then examine average client tenure. Long-standing clients with consistent service history are generally more stable. Also, determine opportunities for upselling or cross-selling to add more revenue.

Review engagement letters to confirm that scope, pricing, and renewal terms are documented. Verbal agreements or outdated letters increase risk.

Step 6: Legal and Compliance Review

Before you finalize value discussions, ensure there are no hidden liabilities, lawsuits, or potential claims.

Verify firm licensing status and CPA credentials and confirm compliance with state board regulations. Ensure clean standing with IRS e-file requirements, and review insurance policies to. Then inspect engagement letters, client contracts, leases, vendor agreements, and software contracts.

Step 7: Valuation & Deal Structure

After diligence, determine a reasonable purchase price and structure.

Select a valuation method and review comparable sales in your region. Decide whether the transaction will be structured as an asset purchase, stock purchase, merger, or buy-in arrangement.

And for the payment model, agree on whether to pay upfront cash, earn-out based on retention, seller financing, or a hybrid method. Seller financing or earnouts can align incentives and protect you if clients leave.

Step 8: Negotiation & Letter of Intent (LOI)

Once you agree on general terms, you document them in a Letter of Intent (LOI). The LOI outlines the purchase price, payment structure, transition expectations, the duration of the seller’s post-sale involvement, and non-compete and no-solicit requirements.

While not always fully legally binding, the LOI sets expectations and reduces misunderstandings during final contract drafting.

Step 9: Final Due Diligence

Before closing, confirm everything one more time.

Audit client files in detail. Verify major engagements and staff agreements. Review all software and login credentials and inspect backup systems, servers, and cloud environments. Reconfirm financial figures against original documentation and confirm all liabilities are disclosed with no outstanding legal issues.

If new risks appear, revisit valuation or structure before signing final documents.

Step 10: Transition Planning

Create a written transition plan that includes how and when clients will be informed, how staff roles will shift, and how systems will be integrated.

Schedule knowledge transfer sessions with the seller, and migrate documents and data securely. Set up access to all software platforms, transfer licenses and subscriptions, and integrate workflows in your system (e.g Financial Cents). Also, update engagement letters under your firm’s name.

Step 11: Closing the Deal

Closing formalizes the transfer of ownership. At this point, sign the final purchase agreement, transfer funds, confirm receipt, and operational control transfers to you.

Complete legal registrations or entity updates and transition payroll and HR documents for acquired staff. Remember to finalize marketing updates (website, email signatures, branding) to reflect the transition.

Step 12: Post-Acquisition Integration

In this final stage, prioritize early outreach to key clients. Monitor retention and revenue performance during the first 90 days and track financial performance compared to projections.

For staff, conduct regular team meetings and set expectations and assign clear ownership for each client and service line. Monitor deadlines closely during the first few months, track client retention and staff morale and address issues quickly.

Buying an Accounting Practice

Where to Find Practices for Sale

You can find accounting practices for sale through several channels. To increase your chances of finding the right fit, use multiple sources at the same time rather than relying on just one.

Practice Brokers and Marketplaces

Professional accounting practice brokers specialize in connecting buyers and sellers. These intermediaries often maintain confidential listings that aren’t publicly advertised and can help with valuation, deal structuring, and due diligence coordination.

There are dedicated brokers like Accounting Practice Sales, Poe Group Advisors, and Accounting Firm Sold that focus exclusively on accounting practices and assist buyers in finding suitable firms across regions.

In addition to brokers, there are online marketplaces where buyers can browse accounting practices listed for sale. Platforms such as the Accounting Practice Exchange allow buyers to search listings based on criteria such as revenue range, services, staff size, and work mode, and connect with sellers confidentially.

Using brokers and marketplaces together increases your reach. Brokers can surface opportunities before they go public, while marketplaces show you firms currently open to acquisition.

CPA Firm Networks and Associations

Industry associations, CPA networks, and professional groups can be excellent sources of lead acquisition. While they may not directly list practices for sale, they connect you with a broad network of practitioners who may be considering retirement or selling in the near future.

Start with your state CPA society and any local accounting associations you’re part of. Many state societies have member directories, classifieds, or partner programs that facilitate introductions between buyers and sellers.

Direct Outreach To Retiring Owners

Direct outreach can produce the best-fit deals, but it requires patience. Many owners don’t list their practices publicly. They may be open to selling in the next year or two, but they haven’t started the process.

Start by identifying firms that meet your acquisition criteria, then reach out directly to the owner. A simple, respectful introduction outlining your interest, experience, and growth plans can open conversations that brokers might otherwise miss. This works particularly well with local firms or niche shops where acquisition activity is low and owners haven’t yet considered listing publicly.

Industry Conferences and Referrals

Accounting conferences are underrated for deal sourcing because they put you in the same room as owners who are thinking about growth, succession, and exit planning. Some won’t reveal their firm is for sale publicly, but many will talk openly about their retirement timeline and whether they have a successor.

This is also where referrals happen naturally. If you build relationships with other firm owners, lenders, attorneys who work with professional services, and practice management consultants, they can introduce you to sellers before a listing goes live.

When attending events, be clear about what you’re looking for. Specific criteria make it easier for others to connect you with appropriate opportunities.

Internal Succession Opportunities

Sometimes the best acquisition isn’t an external one but a succession opportunity within your own firm or team.

If a senior partner or manager is ready to assume ownership of a segment of the firm, or if a buy-in arrangement is possible, this can expand capacity without the disruption of acquiring an outside practice.

Internal succession reduces integration risk because culture, systems, and client expectations are already aligned. It can also strengthen leadership continuity and long-term stability.

While it differs from a traditional external acquisition, it remains a valid pathway for growth.

Common Mistakes When Buying

Here are the most common mistakes buyers make and what to do instead.

Overestimating Client Retention

A frequent mistake is assuming clients will automatically stay after the sale. Many buyers underestimate how much individual relationships, service expectations, and perceived value influence whether clients stay. If you assume retention will be high without a solid communication and continuity plan, you may be disappointed when clients start leaving.

Instead, build a retention strategy early. Introduce yourself to key clients before closing, explain how services will continue or improve, and show a concrete plan for ongoing support.

Underestimating Owner Dependency

Many sellers have built their client base through personal relationships, reputation, and trust. In those cases, the practice is often inseparable from the owner. Acquiring such a practice can be risky if you do not plan for how relationships will transfer to your leadership. Staff and clients might leave once the owner exits, due to the relationship they have with the owner.

Acquiring such a practice can be risky if you do not plan for how relationships will transfer to your leadership.

To counter this, assess how much the business depends on the seller early in due diligence. Check how many different people interact regularly with clients, what client communication habits look like, and whether the seller is willing to support introductions and joint meetings during the transition period.

Ignoring Workflow and System Gaps

Buyers often spend the most time on financial due diligence and not enough time on the practice’s operations. Then they close the deal and discover that the acquired practice runs on scattered spreadsheets, email threads, inconsistent file storage, and undocumented processes.

So, treat workflow and systems as part of valuation. Before signing, check how tasks flow, how deadlines are tracked, how work is reviewed, and whether tools are standardized.

A firm with well-defined accounting processes and modern systems reduces onboarding risk and creates consistency for clients and staff alike.

Poor Communication With Staff and Clients

When communication is poor or reactive, staff and clients get anxious. The former might worry about job security or changes in expectations, and the latter might fear loss of service quality.

To avoid this, develop a communication plan well before closing. Explain the why and how of the transition, set expectations for what will stay the same, and share clear timelines. Regular updates help reduce uncertainty and build trust in the new leadership.

No Post-Acquisition Integration Plan

Perhaps the biggest mistake is assuming the deal closes and then integration will happen naturally. It doesn’t. In fact, integration is where most acquisitions falter. Small issues like duplicated tools, inconsistent client service, unclear task ownership, and teams operating in parallel instead of as one firm compound.

Develop an integration plan that covers systems, workflows, client service consistency, staffing roles, and performance expectations. Without it, you can lose the very revenue and people who made the acquisition attractive in the first place.

The Technology Foundation You Need After Buying a Practice

The biggest risks in acquisitions often come from poor execution during the transition.

Without the right technology foundation in place, disconnected systems, unclear processes, and fragmented client data can quickly lead to missed deadlines, frustrated staff, and clients leaving.

That’s why your first priority post-close should be building a technology foundation. This gives your team a place to find information, a standard way to deliver recurring work, and a single source of truth for who owns what and when it’s due.

An accounting practice management software like Financial Cents supports this foundation by bringing tasks, communication, documents, and deadlines into a single system.

Here’s what that foundation should enable:

Centralize All Client Information, Documents, and Communication in One System

During integration, people waste time when they can’t quickly find the information they need or answer basic questions.

Financial Cents CRM feature keeps client tasks, documents, emails, and notes in one place, so you’re not hunting across email threads, shared drives, chat messages, and spreadsheets.

This reduces handoff errors and ensures anyone can access the information they need easily.

Standardize Workflows Across Both Practices

Two firms may offer the same services but deliver them differently. If the acquired practice uses one way of tracking bookkeeping close tasks and your firm uses another, your team will struggle to collaborate, which can cause mistakes.

Standardizing workflows ensures consistent service quality.

A practice management platform should let you document how you deliver work and reuse that documentation. With Financial Cents, for example, you can convert your firm’s processes into templates so both teams can use them, ensuring everyone follows the same process and your service quality doesn’t decrease.

Assign Clear Ownership for Transition Tasks and Ongoing Client Work

Ambiguity is one of the most common integration problems. After a deal closes, staff want to know who’s handling what, and clients want to know who their primary contact is. Without clarity, work stalls and you might miss deadlines.

Financial Cents allows you to assign ownership to tasks, so team members always know what they’re responsible for, and you can step in if something is blocked.

This matters even more when you’re integrating staff from the acquired firm. Clear ownership reduces confusion and helps new team members understand exactly what they’re responsible for from week one.

Track Deadlines, Workloads, and Progress During the Integration Period

Missing deadlines is one of the fastest ways to lose client trust after an acquisition. If tax returns come in late or a monthly close cycle drifts, clients start wondering whether the firm is still reliable.

Good technology gives you visibility into upcoming deadlines across all clients, who is responsible for each deliverable, your team’s workload distribution, and progress on ongoing projects.

Financial Cents, for example, combines deadlines, task progress, and team assignments into a single view, making it easy to balance workload, shift resources, and keep things moving smoothly during the transition phase.

Maintain Service Consistency During Change

Clients expect that even if ownership changes, service quality should not decline.

A good technology foundation helps both teams operate within the same workflows, communication standards, and client portal. When everyone follows the same processes and tracks work in the same system, service delivery becomes more predictable.

That structure supports consistency while staff and clients adjust to the transition.

Build a Technology Foundation With Financial Cents

Buying an accounting practice can be a transformative move when you do it intentionally. It can fast-track growth, add recurring revenue, and expand your capacity, without waiting years for organic growth to catch up.

But equally important is what happens after closing. Many buyers underestimate how much the success of an acquisition depends on execution during the transition period. Disconnected systems, unclear workflows, and fragmented client data make it harder to retain clients, frustrate staff, and slow down service delivery.

That’s why having the right technology foundation matters. A practice management platform like Financial Cents helps you centralize client information, standardize workflows, assign clear ownership for tasks, and track deadlines and progress.

Ready to build a stronger foundation for growth? Explore Financial Cents today.