Whether you’re just about to launch your accounting firm or you’re already a couple of years in, writing a business plan is one of the most useful things you can do for the firm.

A lot of firm owners skip it because there’s always something more pressing: finding clients, delivering client work, or managing deadlines. But operating without one leaves you without a framework for your most important business decisions, and that eventually shows up in the type of clients you take on, your pricing, and your hiring.

An accounting firm business plan doesn’t have to be a 60-page academic exercise. It can be a practical 10 to 17-page document you’ll actually use and revisit as the firm grows.

We share everything you need to know to write one: what each section should include, accounting-specific examples and prompts, and a downloadable accounting firm business plan template you can start filling in today.

TL;DR

- An accounting firm business plan is a document that defines who your firm serves, what it sells, how it prices, how the work gets done, and what growth looks like over the next few years.

- For most small firms, 10 to 17 pages is plenty. You don’t need a 60-page document that you might not revisit.

- A good plan covers ten sections: executive summary, company overview, market analysis, organization and management, services and pricing, marketing and sales strategy, operations and technology plan, financial plan and projections, risk management and compliance, and an appendix for supporting documents.

- Your revenue forecast is only as real as your team’s capacity to deliver the work behind it. So forecast both together, not separately.

- After writing your business plan, execute it with practice management software to turn the plan into daily workflows your team can run.

- The best business plan is one you’ll actually re-open and reference for decisions on hiring, growth, and pricing.

What Is an Accounting Firm Business Plan?

A business plan is a document that lays out what your company does, who it serves, how it makes money, and how it delivers the work. Unlike a generic one, an accounting firm plan covers specific areas that are relevant to accounting practices, like pricing model, service mix, tech stack, workflow, and capacity planning.

That said, not every situation requires a traditional plan as they take more time to write, often run dozens of pages, and are usually required by investors or VCs.

More often than not, a focused plan of around 10 to 17 pages that covers the essentials is better for an accounting, bookkeeping, or CPA firm. It’s faster to write, and is far easier to reference six months down the line than something exhaustive that you write and forget soon after.

Why Accounting Firms Need a Business Plan

A good business plan offers several benefits. Here are some.

It Helps You Avoid Bad-Fit Clients

When you haven’t defined who you serve, you say yes to everyone. That’s how you end up with a roster of clients who underpay you, cause scope creep, and take up too much time and resources.

A plan defines your ideal client up front, which makes it far easier to recognize and turn down the ones who don’t fit. Kelly Rohrs, CPA, shares how, when she was just starting her firm, she had to turn down one of her biggest clients because they weren’t a good fit: “The fee wasn’t right. The fee should have probably been double. I was putting so much time and energy into it, and there were some ethical questions in regards to what the client was doing or participating in. I knew it wasn’t a good fit, but it was probably the most difficult decision that I had to make at the beginning,” she says.

It Helps You Choose a Profitable Niche

Instead of being a generalist who competes on price and takes whatever comes through the door, writing a plan helps you identify a niche where your expertise is worth more, the work is repeatable, and clients are willing to pay a premium.

It helps you price intentionally

A plan is where you work out your pricing model, whether that’s hourly, fixed-fee, or value-based, or a mix. It’s also where you set your minimum fees and engagement terms, so you’re not taking on clients that cost more to serve than they bring in.

It Builds Repeatable Operations

Your plan documents how work gets delivered and the tech stack that supports it. That means work gets done the same way every time, regardless of who’s handling a particular client, making it easier to scale your firm.

It Lets You Hire Deliberately

Many firm owners hire reactively, waiting until they’re already buried in work before they bring someone on, which often results in a rushed, bad hire. A business plan accounts for hiring from the start, so you know which roles you’ll need, in what order, and at what point to bring them on.

It Reduces Founder Bottlenecks

A business plan is where you design the firm so it doesn’t depend entirely on you. You define roles, assign ownership of workflows, and set up systems so the team can keep projects moving and make decisions even when you’re not available.

The 10 Sections Every Accounting Firm Business Plan Should Include

A business plan for an accounting firm should include the following sections:

- Executive Summary: A one-page summary of the whole plan, covering what the firm is, who it serves, and where it’s headed.

- Company Overview: Information about your business and your objectives.

- Market Analysis: Overview of your industry, target clients, and competitors.

- Organization & Management: Your founder bio, current team, and hiring roadmap.

- Services & Pricing: The services you offer and your pricing model.

- Marketing & Sales Strategy: How you’ll attract leads and close them.

- Operations and Technology Plan: Your workflows, capacity planning, and tech stack.

- Financial Plan & Projections: Your revenue model, expenses, and profit projections.

- Risk Management & Compliance: How you’ll handle compliance, data security, insurance, and internal controls.

- Appendix: Supporting documents and detailed information that backs up the main plan.

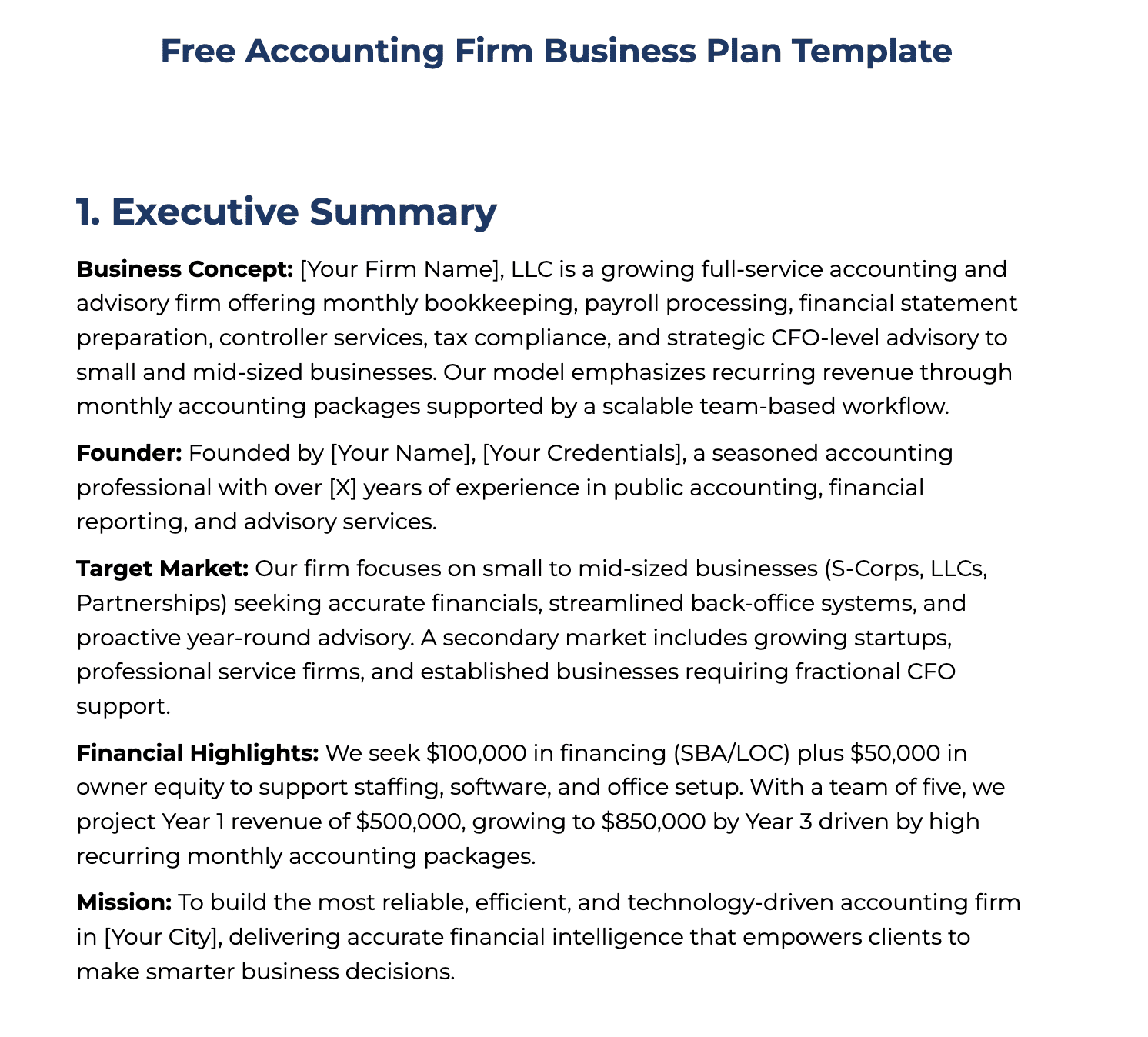

Section 1: Executive Summary

This is usually the section you write last, since by then you have a holistic view of the plan and can summarize it properly. But it appears first in the business plan, so anyone can quickly understand what the firm is, who it serves, what it offers, and where it’s headed financially before diving into the details.

Keep it to one page. Any longer and it stops being a summary that the reader can take in at a glance.

Pro tip: Include one or two lines on what specifically sets your firm apart from the other accounting, CPA, or bookkeeping firms competing for the same clients. This can be your niche, technology, service mix, or experience.

For example, a differentiation line for a SaaS-focused firm might read:

“Our founder spent the last 10 years as an in-house controller at two Series-A SaaS companies before starting XYZ Bookkeeping. That experience means we already understand how SaaS businesses operate, where the financial reporting gets complicated, and what good accounting looks like for a company at that stage.”

Section 2: Company Overview

The next section in your plan is the company overview, sometimes called the company description. It runs one to two pages and covers the firm’s foundational details: accounting business name, legal structure (LLC, S-corp, sole proprietor, or partnership), ownership, location, vision, firm history if you’re already operating, and key objectives for the year ahead.

To make this section even more relevant, add your state-board-of-accountancy restrictions (if any), working model (remote, hybrid, or in-person), and founder story.

Section 3: Market Analysis

Next, write an analysis of the market you’re operating in. This should be about two pages and four sub-parts: industry overview, target client profile, competitive analysis, and Strengths, Weaknesses, Opportunities, Threats (SWOT) analysis.

For the industry overview, always use real data to back up your points. This keeps the section credible and shows a lender or partner that your plan is grounded in reality. You can pull industry size and growth figures from sources like the AICPA, Accounting Today, and BLS data.

And if you’re a small to mid-sized firm, the Financial Cents Accounting Firms Revenue Report is especially useful for benchmarking. It surveys almost 300 firm owners and breaks down how much they earn, which services drive the highest revenue, which carry the best profit margins, and how revenue is distributed across firms of different sizes. This is also where you state your accounting niche, but be specific. Instead of saying “tech startups”, say “Series-A SaaS startups, $1–10M ARR, 10–50 employees.”) And once you’ve defined your niche, stick to it.

Many firm owners who don’t end up regretting it. As Tonya Schulte shares:

Section 4: Organization & Management

This section covers staffing, both current and future. A page is enough, and it includes your founder bio, key hires planned, organizational structure, and hiring philosophy.

Keep the founder bio to one paragraph, focused on credentials and relevant experience. A lender or future partner reading this wants to know you’re qualified to manage the firm. Lead with your designation, your years in the field, and the experience directly relevant to the firm you’re building. For instance: “Founded by Jane Doe, CPA, with twelve years in public accounting, including six years leading the small business practice at a regional CPA firm.” That tells a reader a lot about your suitability for the role.

Note: Clarify the type of team you want to hire, whether offshore or all-domestic, so you can put the right structures in place.

Section 5: Services and Pricing

This section answers two questions: what does your firm sell, and how do you charge for it? It runs about two pages, split into services offered and pricing model.

For the services to offer, Roger Knecht, President of Universal Accounting Center, recommends these 3 core services, grouped into categories: Bookkeeping and accounting, tax prep and tax planning, and CFO and advisory services. And as a small firm, you don’t have to deliver all of these yourself. Roger suggests collaborating with other professionals and firms that handle services you don’t, and vice versa:

For your pricing model, choose between hourly, fixed-fee, and value-based, and explain why. You can also choose more than one pricing model. For instance, a firm serving construction companies might use fixed-fee pricing for monthly bookkeeping, hourly billing for tasks such as staff training or projects with an undefined timeline, and a value-based quarterly fee for advisory services.

Need more help with setting pricing? Here’s a free bookkeeping pricing template sample and an accounting and bookkeeping services pricing calculator.

Section 6: Marketing and Sales Strategy

This is another 1-2-page section on how to get clients: channels, lead-generation plan, sales process. Marketing channels you can try include referrals, networking, SEO & content marketing, LinkedIn personal brand, paid ads, and strategic partnerships.

You don’t have to start all these marketing channels at first; just pick 2 or 3 you can actually commit to, and in time, you can add others.

In addition to marketing, you need sales. Marketing gets you the leads, and sales converts them.

The usual sales process for accounting firms is lead → discovery call → proposal → engagement letter → onboarding, and each step is important.

Note: The accounting proposal and the accounting services engagement letter are documents you’ll use in every deal, so build them once and reuse them for every prospect. Just ensure to tailor it to each engagement’s peculiarity.

You can build them as templates and store them in Financial Cents so everyone can access them.

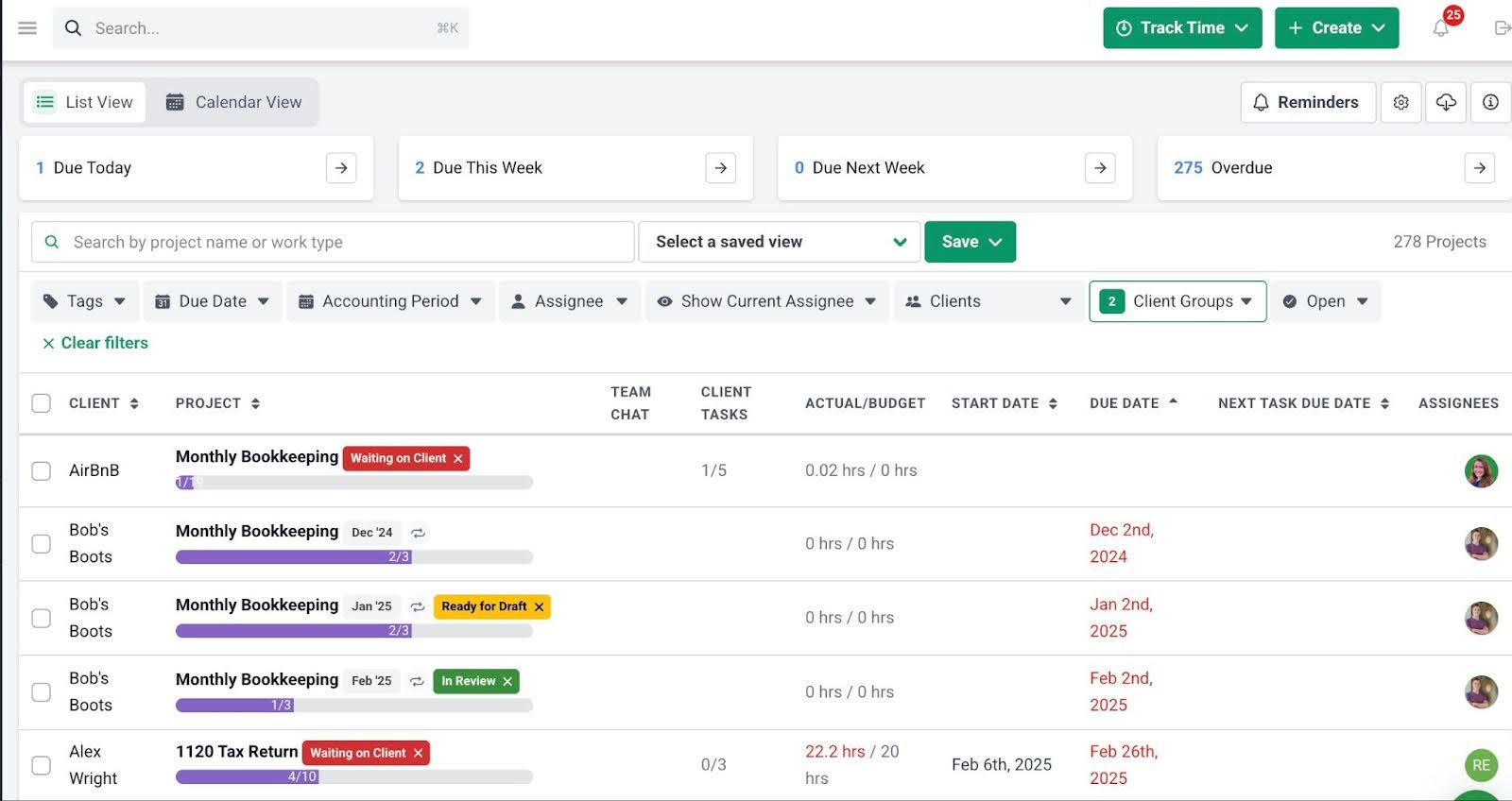

Section 7: Operations & Technology Plan

The next thing to address in your plan is operations and technology. This covers your tech stack, your workflows/engagement delivery, your accounting team and client communication, and capacity planning.

It’s important to include your workflow in your plan, as it can affect the firm’s success. Financial Cents’ 2025 State of Accounting Workflow and Automation Report found that 55.5% of firm owners still experience workflow inefficiencies.

A documented workflow helps you build a self-operating accounting firm. It means you can delegate and work gets done the same way every time, regardless of who’s doing it. At a minimum, document your standard month-end close, year-end, and tax engagement workflows.

Also, outline your tech stack, organized by function. A standard firm has accounting software, tax prep software, practice management software, accounting document management system and e-signature tools, communication tools, and payroll software.

Section 8: Financial Plan & Projections

This is the numbers section. It runs two to three pages and covers revenue model, expense model, profit and cash flow projections, and funding needs.

Start by calculating a revenue projection for each service line. Do this in a table that includes the service, average fee, number of clients or units, and projected revenue, using a simple formula: average revenue per client × target client count = projected revenue. Build it for Year 1, then project Years 2 and 3 based on your hiring plans and accounting firm growth strategies.

Here’s a sample Year 1 revenue projection for a CAS firm:

| Service | Avg fee | Units | Revenue |

|---|---|---|---|

| Bookkeeping – Starter | $500/mo | 20 | $120,000 |

| Bookkeeping – Standard | $900/mo | 15 | $162,000 |

| Bookkeeping – Advanced | $2,000/mo | 5 | $120,000 |

| Payroll | $150/mo | 25 | $45,000 |

| Advisory / CFO | $175/hr | 250 hrs | $43,750 |

| Tax Add-ons | $650 | 30 | $19,500 |

| Total Revenue | ~$510,000 |

Note: Always account for client churn in your revenue projections. It’s impossible to retain every client you’ve ever had.

Next, create an expense model and list all your costs. The usual expenses for an accounting firm are software stack, salaries, insurance, marketing, and office space (if applicable).

Then share your profit and cash flow projections. Subtract your cost of goods sold from revenue to get gross profit, then subtract operating expenses from total revenue to get your net profit.

Finally, state how you’ll fund the firm. You can either bootstrap, take an SBA loan, or buy an existing accounting practice.

Section 9: Risk Management & Compliance

Accounting firms handle sensitive financial data and operate under professional regulations, which means you carry real liability when something goes wrong. That’s why you need a risk management and compliance section. It should cover three areas: compliance and quality control, insurance and risk coverage, and internal controls and operational safeguards.

First, spell out how you’ll keep work accurate and compliant. For instance, you’ll need a Written Information Security Plan (WISP), which the IRS requires of tax firms and which sets the rules for data handling, passwords, device use, and breach response.

Next, list the risk areas your firm will carry coverage for and what each protects against. One insurance you shouldn’t skip is Errors & Omissions (E&O). This is the coverage that protects you from mistakes in your work that can turn into a claim that threatens your entire practice.

Finally, note the internal controls that keep the firm accountable and protected. For instance, use software like Financial Cents that maintains audit trails, logging edits, approvals, and document access so there’s a traceable record behind every client deliverable.

Section 10: Appendix

The appendix is where you put all supporting details and proof to keep the main plan clear and focused. Common things to include are founder and leadership bios, with certifications and licenses, a sample engagement letter and standard service agreement, a draft pricing sheet, your target client list or pipeline, references, and your WISP summary.

Read: How to Start an Accounting Firm

Free Accounting Firm Business Plan Template

We’ve put everything in a ready-to-use template you can download and fill in today. It covers all ten sections, with prompts and examples for accounting and bookkeeping firms. It is available in Word and Google Docs format.

Download your free business plan templateHow to forecast revenue and capacity for an accounting firm

Your revenue forecast is only as real as your team’s capacity to deliver the work behind it. So forecast both together, not one and then the other.

To do this, you’ll need the basic planning inputs like number of clients, average monthly fee, service mix, one-time projects, tax-season spikes, billable capacity, staff cost, software cost, marketing spend, and churn and retention assumptions.

Once you have these, you can then build the forecast. Multiply clients by fee, one line at a time:

| Service | Clients | Rate | Monthly Revenue |

| Monthly bookkeeping | 20 | $500/month | $10,000 |

| Advisory | 4 | $750/month | $3,000 |

| Payroll | 12 | $150/month | $1,800 |

| Cleanup (one-time) | 2/month | $1,200 | $2,400 |

| Total | $17,200 |

This comes to $206,400 a year before churn.

Now, remember what we said earlier about how the revenue forecast isn’t accurate until you account for the capacity of the people doing the work? For every line in the table, ask how many hours it takes to deliver and who’s delivering it.

Say that $17,200 of monthly work takes around 150 billable hours to deliver, and one full-time person realistically bills 120 to 130 hours a month, this forecast would need more than one person to get the target revenue.

Be honest about your own capacity as the owner here, too. A plan that only works if you bill 80 hours a week isn’t realistic, because no one sustains that for long.

Also, build a trigger in your forecast. Decide in advance what happens when capacity is full, as you can either hire someone or raise your prices.

Common Mistakes to Avoid When Writing an Accounting Firm Business Plan

There are a few mistakes accountants make when writing their business plan that affect its viability. Here are the ones to watch for:

Vague Target Client

Create an ideal client profile that captures specifics about the business: industry, annual revenue, employee count, the pain points they face, and what they can realistically pay for accounting services. The more defined that profile is, the more your marketing, messaging, positioning, and offer resonates with that exact client.

Pricing Model Copied From Someone Else

Your pricing has to be tailored to your firm, because only you know your clients, capacity, and offerings. Use other firms as a reference point, but set your prices based on your numbers.

Being Too Generic

Your plan should reflect your reality and shape everything from your pricing structure to your onboarding to the software you choose.

Failing To Plan for Capacity

Always account for the time and capacity of the people doing the work. You don’t want to project revenue but not have capacity.

Over-Projecting Revenue, Under-Projecting Time

It’s natural to be optimistic, but most owners overestimate how many clients they’ll land and underestimate how long the work takes. It’s better to plan conservatively and be pleasantly surprised than to build the firm on numbers you can’t hit.

Not Revisiting the Plan Regularly

This is the most common mistake of all. Many owners write the plan once and never open it again. Your plan should be a living document you reference and update as the firm changes.

Ignoring Operations

Plenty of plans cover services and marketing for accountants in detail, but not operations, which actually determine how the firm runs day-to-day.

Execute Your Business Plan with Accounting Practice Management Software

After writing your business plan, you need to execute it. And for that, you need accounting practice management software like Financial Cents. It can help turn those decisions into daily operations and repeatable work. Here’s how:

- Recurring Projects: You can set projects to recur each month or quarter, so you don’t have to create them from scratch every time.

- Workflow Templates: Document your workflows (like month-end close or payroll) as templates you can store and reuse in the software, which ensures consistency and saves time.

- Client Requests: Easily request documents from clients and automate the follow-up, instead of manually chasing them. This increases efficiency and helps you meet deadlines.

- Team Assignments: Assign tasks to team members with clear responsibilities, so everyone knows what they’re supposed to do and projects keep moving.

- Deadline Tracking: Set and assign deadlines on every project, visible to everyone, so nothing falls through the cracks.

- Client Portal and Document Management: Store and manage documents in a single client portal, so both clients and team members can easily find what they need.

- Time Tracking: Track how long work actually takes, so you can bill accurately and properly account for capacity.

- Billing: Invoice clients with Financial Cents based on the time tracked and the work completed.

- Dashboard Visibility: Get a bird’s-eye view of everything happening in the firm. See who’s working on what, upcoming deadlines, and each team member’s capacity.

This has been particularly useful for our clients like JNW Group, a tax firm with 10 staff and 1,300+ clients. As Jim, a staff member, shares:

We’ve included a downloadable accounting firm business plan template you can use to write your own. Just download it, fill in your details, and you’ll have a working plan in a few hours. Then use Financial Cents to actually execute it.