Bookkeeping disputes do not always start with deliverables. More often than not, they’re a result of unclear agreements.

It starts off innocently; a client assumes monthly reconciliations include payroll. You assume they know it does not.

Scope creep, late payments, unrealistic turnaround expectations, and liability confusion are the problems that quietly derail bookkeeping engagements. And in almost every case, a well-written contract could have prevented them.

In this article, we walk you through how to create a bookkeeping contract agreement that holds up, what to include in each section, and why each clause matters. There is also a free template you can download and customize for your firm.

What is a Bookkeeping Contract Agreement?

A bookkeeping contract agreement is a legally binding document that outlines the terms of your engagement with a client, which services you’ll provide, what each party is responsible for, how fees are structured, how long the agreement runs, and how either side can end it.

A solid bookkeeping service agreement removes ambiguity in a way that goodwill and verbal understanding simply can’t. When a client asks you to do something outside the original scope, you have a document to point to.

Difference Between a Bookkeeping Contract and an Engagement Letter

It’s worth clearing up a distinction that causes confusion: the difference between a bookkeeping contract and an engagement letter.

A bookkeeping engagement letter is shorter, more conversational, and covers the basics: scope of services, fees, and a few key terms written in plain language.

A contract for bookkeeping services goes further. Liability clauses, dispute resolution, confidentiality, data security, termination conditions, and amendments. It’s a full legal document built for the scenario where something goes wrong, and both parties need to know exactly where they stand.

Key Elements to Include in Your Bookkeeping Services Agreement

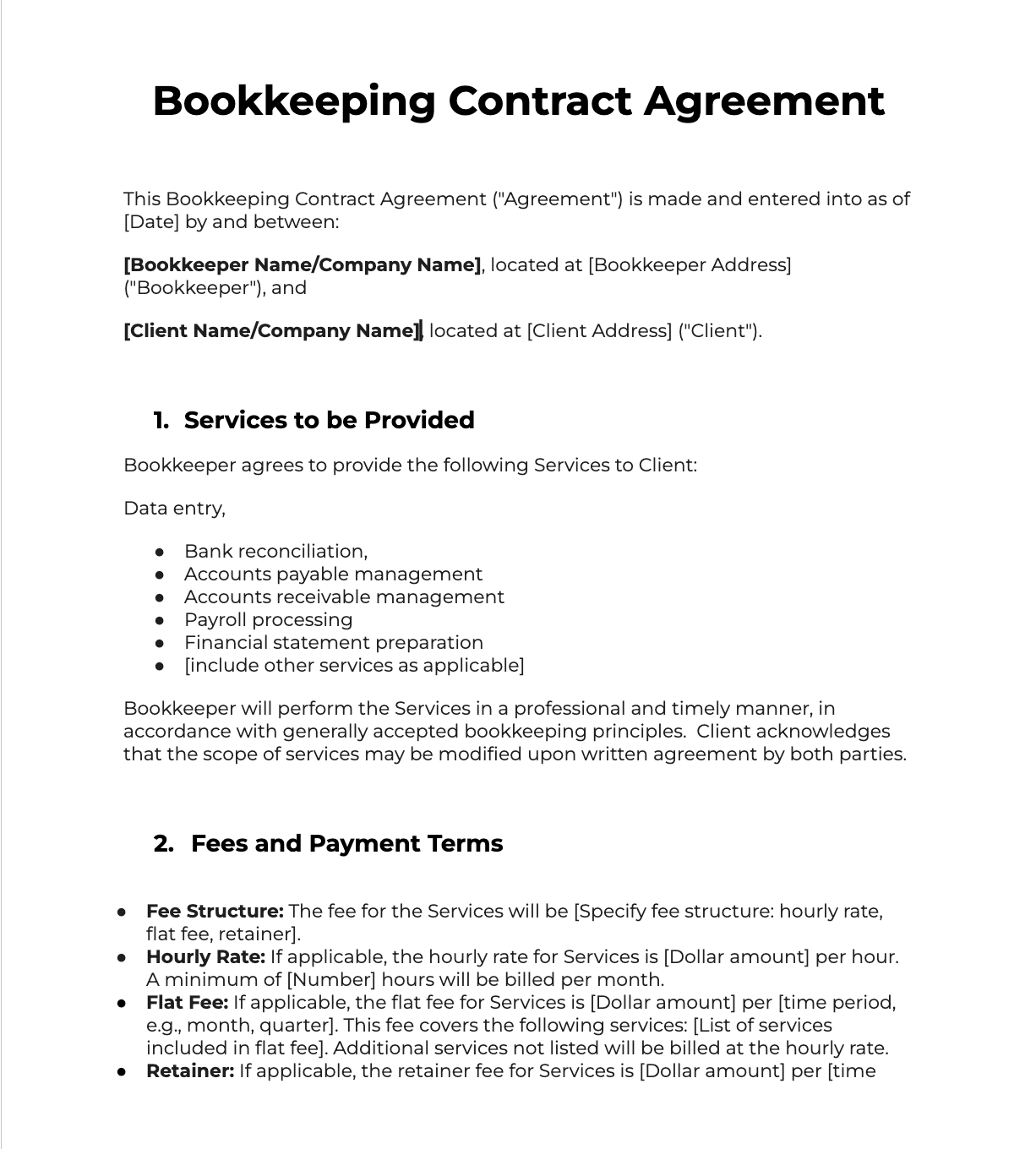

1. Parties Involved

Start by clearly identifying who is entering into the agreement. Include the full legal name of your firm (or your name as a solo bookkeeper), your business address, and the same information for the client. If the client is a business, note the legal business name and the name of the authorized representative signing on their behalf.

This section should also clarify the nature of the relationship, specifically that you are an independent contractor, not an employee. This distinction has tax and legal implications that both parties need to understand from the outset.

2. Scope of Services

List every service you will provide, in as much detail as possible. If you are handling monthly bank reconciliations, accounts payable, accounts receivable, payroll processing, and financial statement preparation, say exactly that. If something is not listed, it is not included. Be specific about:

- Frequency: Is this monthly, quarterly, or annually?

- Deliverables: What will the client actually receive? Reports, reconciled accounts, and a clean general ledger?

- Software: Which accounting platform will be used? Who is responsible for the subscription?

- Out-of-scope work: Consider explicitly noting what is not included, such as tax preparation, audit support, or CFO advisory services.

3. Client Responsibilities

Your ability to do the work depends entirely on the client doing their part, and this section of the contract is where you make that explicit.

It should require them to provide timely access to bank statements, receipts, and financial documents, grant access to the relevant accounting software and systems, respond to requests within a defined timeframe, and take responsibility for the accuracy of the information they hand over.

4. Fees and Payment Terms

Spell out your pricing structure clearly. Whether you charge a flat monthly fee, an hourly rate, or a tiered retainer based on transaction volume, define it explicitly. Vague payment language leads to disputes, delayed payments, and awkward conversations you do not want to have.

At a minimum, this section should cover your fee structure; whether that’s a fixed monthly fee, hourly rate, project-based pricing, or a retainer, alongside your billing cycle, late payment terms, who is responsible for engagement-related expenses like software subscriptions and filing fees, and your right to adjust fees with reasonable notice if the scope expands or annual pricing changes apply. The more specific you are here, the less room there is for a client to claim they didn’t know what they were agreeing to.

For more on structuring your pricing before you get to the contract stage, the bookkeeping pricing template guide and how to price bookkeeping services are worth reviewing.

For fixed rate or value-based pricing, Alexis Sadler, CEO of Accounting Therapy, suggests considering factors like the number of monthly transactions, reconciliation time, and complexities:

I look at the number of transactions in a month. I figured a minute per transaction, and then I averaged 15 minutes for reconciliation. But then I look at are we doing any specific journals that require us to get out of apps? Are we doing app support? Are we onboarding and onboarding employees? Because they have high turnover? [I look at] Those kinds of things as well. But my basic is a minute per transaction and 15 minutes per reconciliation"

5. Confidentiality Clause and Data Security

Bookkeepers handle some of the most sensitive information a business has, and your contract needs to reflect the weight of that responsibility.

A strong confidentiality clause should state that all client financial information will be kept strictly confidential, that you won’t disclose anything to a third party without written consent, and that those obligations survive the termination of the agreement, meaning they don’t expire the moment the engagement ends.

Beyond confidentiality, it’s worth addressing data security directly, particularly if you’re storing client files digitally or working across cloud-based accounting practice management platforms. Define how the data is stored, who has access to it, and what happens to it when the engagement wraps up, whether that means returning it, deleting it, or archiving it.

6. Term and Termination

Every contract needs a defined start date and a clear explanation of how it ends. Specify whether the agreement is month-to-month, fixed-term, or ongoing with annual renewal, and if there’s a minimum commitment period.

For termination, define how either party can exit and consider whether the notice period should differ depending on who’s initiating it. Include language requiring payment of all outstanding invoices upon termination and the return or transfer of all client documents and data.

7. Dispute Resolution

When disagreements happen, having a defined process for resolving them saves both parties significant time, money, and stress.

Most bookkeeping contracts specify arbitration rather than litigation. Arbitration is typically faster and less expensive than going to court, and it keeps disputes private. Your clause should specify:

- The method of resolution (arbitration, mediation, or litigation)

- The jurisdiction or state law that governs the agreement

- Who bears the cost of arbitration or legal proceedings

If you are using arbitration, specify that the decision is binding and enforceable.

8. Limitation of Liability

This clause protects you from being held responsible for damages that go beyond the value of your services. Even with the best practices and professional care, errors can happen.

A standard limitation of liability clause states that in no event will your liability exceed the total fees paid by the client in the preceding contract period, or the limits of your professional liability insurance, whichever is greater.

This does not mean you are absolved of responsibility for negligence. It simply caps the financial exposure to something proportionate, rather than leaving you open-ended to unlimited claims.

9. Amendments

As client needs evolve, your services will too. This section explains how changes to the agreement are made, and makes clear that verbal agreements do not count.

Standard language states that any amendments must be made in writing and signed by both parties. This keeps your original scope of services intact unless both parties formally agree to change it, which prevents scope creep from quietly becoming an expectation.

10. Signatures and Date

The contract isn’t binding until both parties have signed and dated it, so include a signature block for yourself (or an authorized representative of your firm) and for the client. Once it’s executed, make sure both of you retain a copy.

Free Bookkeeping Contract Services Agreement Template

Below is a customizable bookkeeping service agreement template you can adapt for your firm. It covers all the essential sections outlined above. You can download it and also receive a Google Docs copy sent directly to your inbox.

Best Practices for Creating a Contract for Bookkeeping Services

Here are some tips to keep in mind when creating a bookkeeping contract.

Use Clear and Concise Language

Avoid legalese and complex jargon. Your contract should be easy to understand for both you and your clients. Use plain language and straightforward sentence structure. If you must include any technical terms, provide clear definitions within the contract itself.

Maintain Professional Formatting

First impressions matter, and a professional-looking contract makes a positive statement. Use a professional font and layout that is easy to read and navigate. In addition, make the formatting consistent throughout the document with clear headings, bullet points, and proper spacing.

Proofread Carefully

Typos and errors are sloppy and undermine the professionalism of your agreement. Before finalizing and sending the bookkeeping contract to the client, proofread it meticulously for any mistakes. It’s also advisable to have someone else (like a team member or professional editor) review the document for any errors you might have missed.

Review and Update Regularly

Your business and client needs may evolve over time. It’s essential to review your bookkeeping contract agreement periodically, at least annually, so it reflects your current services and pricing structure.

Alexis also advises to evaluate your fixed pricing regularly. She says “We have a process to do the 90 day evaluation, the six month evaluation, and then we evaluate every year just on an anniversary basis. So we are always evaluating that number.”

If you feel there’s any need for change, update the agreement and sign the revised version with your client.

Simplify Your Bookkeeping Service Agreement Through E-Sign

You no longer have to print, sign, and mail physical copies of contracts. Many online tools now offer a secure and convenient e-signature feature to streamline the agreement process.

Financial Cents, an accounting and bookkeeping practice management software, for example, provides an e-signature integration with Adobe Sign which allows you to:

- Upload your bookkeeping contract template directly to the platform.

- Send the contract electronically to your client for review and signature.

- Receive instant notification once your client has signed the agreement.

- Securely store signed copies of the agreement for both you and your client.

This streamlines the signing process, saves time, and ensures both you and your client have a readily accessible copy of the signed agreement. With this feature, finalizing your bookkeeping contracts becomes effortless and convenient.

Free Bookkeeping Contract Services Agreement Template

Below is a customizable bookkeeping service agreement template you can adapt for your firm. It covers all the essential sections outlined above. You can download it and also receive a Google Docs copy sent directly to your inbox.

Please note: This template is provided for informational purposes and should not be construed as legal advice.

Free Bookkeeping Contract Service Agreement

Why Every Bookkeeping Firm Needs a Strong Contract

Protects Your Business

Without a signed contract, you are exposed. If a client disputes a charge, refuses to pay, or claims your work caused them financial harm, you have little to stand on.

Prevents Scope Creep

A clearly defined scope of services section makes it easy to have that conversation. When a client asks for something outside the agreement, you can simply say, “That falls outside our current scope. I can put together an amendment to add it.”

Establishes Payment Expectations

When payment terms, due dates, and late fee policies are written into the contract and signed before work begins, clients cannot claim they were unaware. It also gives you a documented basis for following up on overdue invoices.

Pairing a strong payment clause with an accounting workflow software, which supports bookkeeping, invoicing, and billing within the same platform you use to manage client work, keeps the financial side of the engagement organized and easy to track.

Builds Professional Credibility

Sending a well-structured bookkeeping service agreement signals to clients that they are working with a professional firm. It sets the tone from the very beginning of the relationship.

Best Practices for Using a Contract for Bookkeeping Services

Review contracts annually

An agreement that was accurate two years ago may no longer reflect what you’re actually doing, so build in a yearly review to make sure it still does.

Update terms as services evolve

If you add payroll services, switch accounting software, or change your billing model, update the contract. Do not rely on verbal agreements or email threads to cover changes. Use the amendments clause.

Always sign before starting work

This one sounds obvious until a client is eager to get started and the contract is still being finalized. Starting work without a signed agreement leaves you unprotected from day one. No signed contract, no work started. Make it a policy and hold the line.

Store contracts securely

Contracts should be stored somewhere centralized, organized, and easy to retrieve. If a dispute arises six months into an engagement, you need to be able to pull the signed agreement immediately.

Sign electronically

Paper signatures are slow, especially when you’re working with remote clients. Electronic signatures are legally binding in most jurisdictions and significantly faster to execute.

Financial Cents includes a built-in proposals and engagement letters feature that lets you send contracts for e-signature directly from the platform. If you’d prefer a dedicated solution, Adobe e-sign is also integrated into Financial Cents and works well if that’s already part of your workflow. Either way, it’s a better option than printing, scanning, and emailing PDFs back and forth.

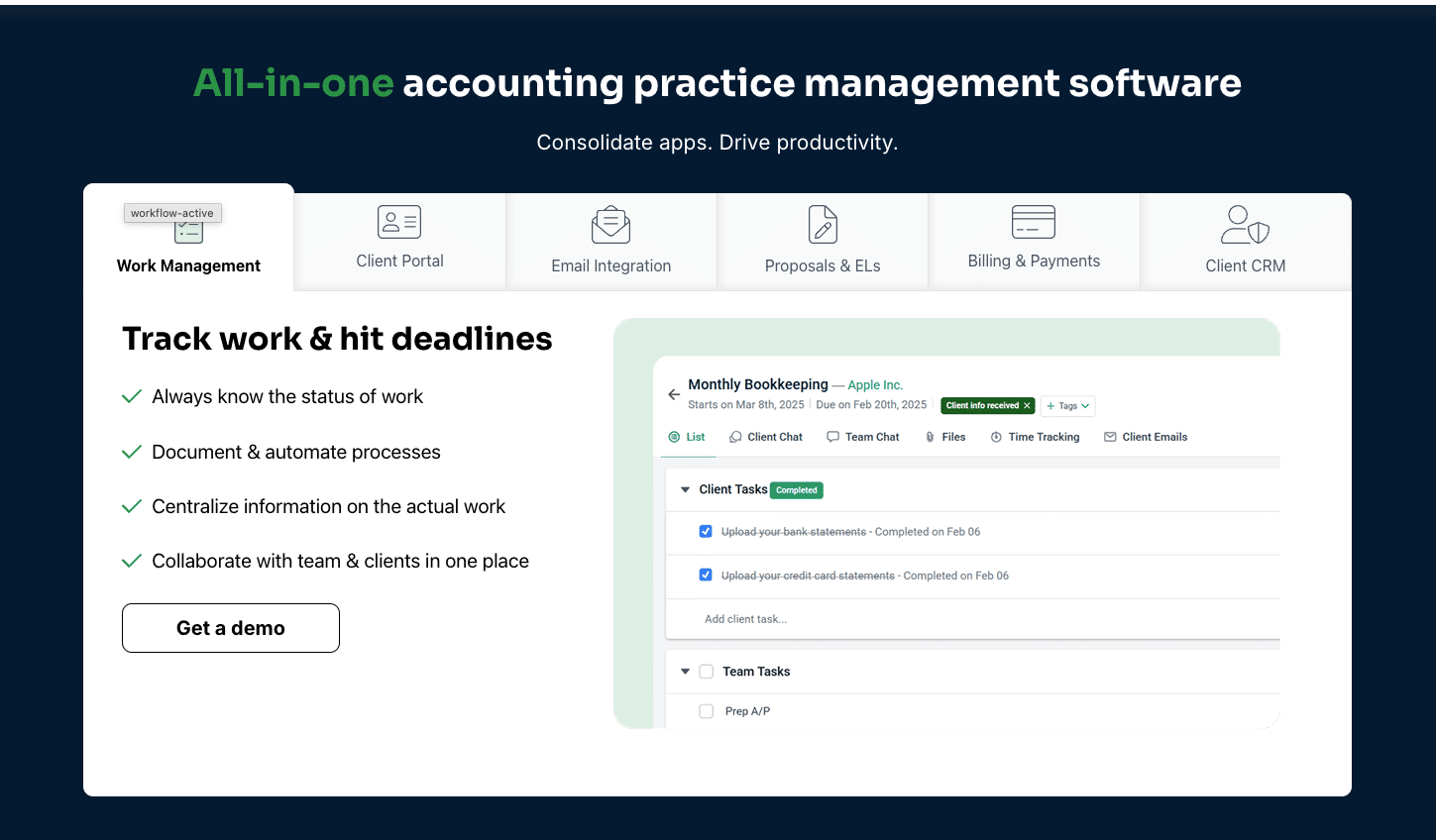

Managing Bookkeeping Clients and Contracts with the Right System

Signing a contract is the beginning, not the end. Once an engagement starts, you need systems to make sure you’re actually delivering what the contract promises. Multiple tools like email threads, shared folders, and spreadsheets create gaps. Nobody has a complete picture of where any given client’s work actually stands.

Financial Cents brings it all into one place. Here’s how it supports the kind of structured engagement a strong contract sets up:

- Centralize client records and agreements: Every client has a dedicated profile storing agreements, notes, contact information, and engagement details, all in one place.

- Tie scope of work to projects and workflow templates: Your contract’s scope maps directly to projects and tasks using bookkeeping workflow templates, so deliverables are built into your bookkeeping workflow, not left to memory.

- Automate billing based on contract terms: Schedule recurring invoices in advance and collect payments without switching between systems.

- Manage client communication and document requests: Structured requests and automated reminders keep clients accountable to their responsibilities under the contract.

- Assign responsibilities to team members: Tasks are assigned with due dates, so accountability is built into the workflow.

- Monitor recurring deadlines and deliverables: Upcoming deadlines across all clients surface in one view, so nothing gets missed.

Conclusion

If your current agreements are vague, outdated, or missing key clauses, now is the right time to revisit them. This template gives you a starting point. Customize it, have it reviewed, and make it a non-negotiable part of your onboarding process before work begins on any new engagement.

Once the contract is signed, the next priority is making sure the work it promises actually gets done. From client records and workflow management to billing and document requests, Financial Cents brings the operational side of a bookkeeping engagement into one place.

Start a free trial and see how it supports the kind of structured, professional practice your contracts are designed to reflect.